Is a U.S.-Only Retirement Strategy Still Safe?

For decades, the traditional American approach to retirement has been straightforward: save diligently, invest in domestic markets, and count on Social Security or pensions to fill in the gaps. This U.S.-centric path worked well in an era of steady economic growth and a dominant dollar.

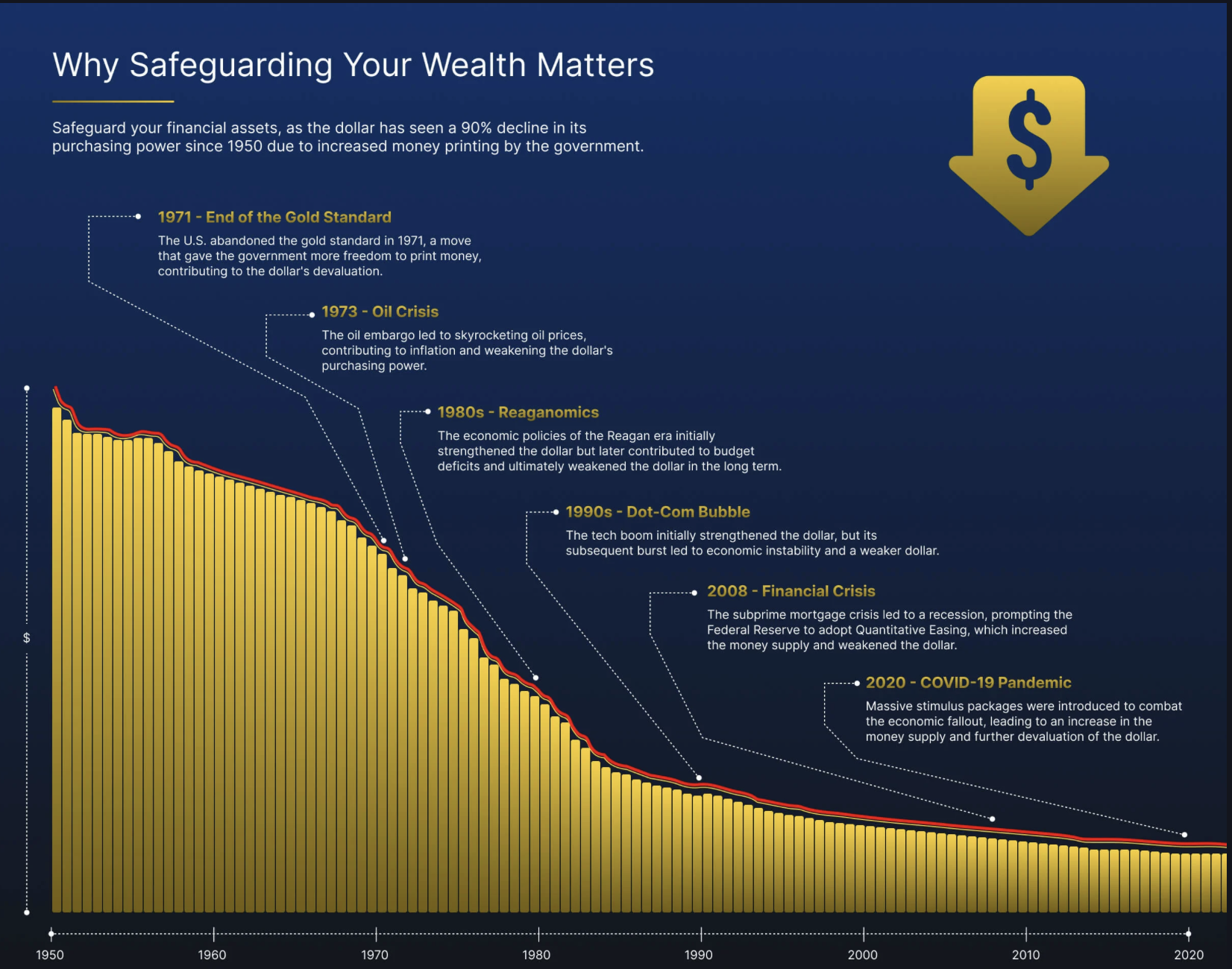

But times are changing. Concerns about economic uncertainty, the ongoing devaluation of the U.S. dollar, and overexposure to a single market have left many Americans wondering: Is keeping your retirement solely U.S.-focused still the safest choice?

The Growing Risks of Staying Domestic

The risks are becoming increasingly clear. Market volatility can quickly erode savings when all your assets move in step with the U.S. economy. Inflation steadily reduces purchasing power, while the weakening of the dollar makes retirement more expensive, particularly for those who plan to spend time abroad. Political and regulatory uncertainty—from tax policy shifts to ballooning government debt—adds another layer of unpredictability. Perhaps most importantly, keeping everything domestic limits access to opportunities in other parts of the world, leaving entire sectors and markets untapped.

Why International Diversification Matters

International diversification offers a way to counter these risks. Spreading assets across global markets adds balance and resilience, reducing the impact of downturns in any single economy. Holding wealth in different currencies helps guard against the long-term decline of the dollar, while investing abroad provides exposure to industries not available in the U.S., such as European healthcare leaders or Asian technology innovators. History has shown that portfolios with global exposure are often more stable during turbulent times.

Source: Bitbo

The Case for Swiss Banking

Switzerland stands out as a particularly strong choice for those seeking to integrate international diversification into retirement planning. The country’s financial system is renowned for stability, with banks among the safest in the world. The Swiss franc is considered a safe-haven currency, offering strength and reliability against the dollar. Strict privacy laws and robust regulatory protections safeguard account holders, giving retirees peace of mind. For Americans, this path is not only possible but fully legal when done with the right guidance, and WHVP specializes in helping U.S. clients establish offshore diversification in full compliance with U.S. regulations.

What to Consider Before Going Global

Before moving assets abroad, it is important to understand the responsibilities involved. U.S. citizens must comply with reporting requirements such as FBAR and FATCA. Working with an advisor who is both SEC-registered and licensed under Swiss regulations is essential. Offshore strategies should always align with broader retirement goals, whether that includes legacy planning, travel, or simply ensuring long-term security. At WHVP, we also coordinate with CPAs, tax attorneys, and estate professionals to make sure every piece of your financial life works together seamlessly.

For many Americans, one of the most effective ways to diversify retirement savings globally is through a self-directed IRA. These accounts can be structured to hold international investments, including offshore bank and brokerage accounts, without triggering a taxable event. By properly setting up the IRA with a qualified custodian, you can move a portion of your retirement assets abroad while maintaining the tax-advantaged status of the account. This allows you to access the benefits of global diversification and currency protection while keeping your retirement planning compliant with IRS rules.

How WHVP Helps Build Global Retirement Plans

Our approach at WHVP is deeply personal and focused on building resilient, internationally diversified portfolios. We tailor strategies to each client, incorporating both asset class and currency diversification, while fostering long-term relationships that extend across generations. With our SEC registration, Swiss regulatory licensing, and transparent fee structure, we provide the trust, independence, and security our clients seek when looking beyond U.S. borders.

Time to Rethink Retirement?

The world has changed, and so have the risks of keeping retirement savings tied to a single country. By expanding your financial horizon, you can create a retirement plan that is more flexible, more resilient, and better equipped to handle whatever the future holds. At WHVP, we have been guiding Americans through this process for more than three decades. If you are ready to explore how international diversification can strengthen your retirement, we invite you to schedule a free consultation and take the first step toward a truly global retirement strategy.

If you’re interested in learning how to benefit from Switzerland’s stable financial environment and gain access to international opportunities, we invite you to schedule a free consultation today.