"Don't Worry", they say...

As we move deeper into the year and look forward to longer days and brighter summer skies, the geopolitical climate remains anything but calm. From a Swiss perspective, grounded, observant, and traditionally neutral, the contrast could hardly be sharper.

Tensions in Eastern Europe have intensified again, with the renewed escalation in Ukraine reminding markets that geopolitical risks rarely move in straight lines. Events close to Europe’s borders are a sober reminder that regional conflicts can quickly create broader economic consequences. At the same time, instability in the Middle East continues to command global attention, underlining how closely geopolitics, energy markets, and inflation remain connected. Whether diplomacy will prevail is still an open question and one markets continue to watch carefully.

Yet, the world is never only serious. Even during uncertain times, there are moments that unite rather than divide. In just a few weeks, the FIFA World Cup will begin across Canada, Mexico, and the United States, offering a welcome distraction and a reminder that competition does not always have to be zero-sum. Switzerland will take the field shortly after the opening matches. Proof that, at least in soccer, neutrality is rarely an option. As always, we cheer not only for talent, but for discipline, resilience, and consistency, qualities investors may also recognize as essential for long-term success.

With that balance in mind, let us turn to the markets: what has moved, what matters, and how we interpret it.

Don’t Worry

Along the lines of Bobby McFerrin’s famous song Don’t Worry, Be Happy, markets appear to be following the same tune:

“In every life we have some trouble

But when you worry you make it double

Don’t worry

Be happy.”

That seems to be the mindset of many investors today. However, a closer look beneath the surface reveals that market performance is once again being driven by only a handful of companies, primarily within the technology sector and, more specifically, semiconductor businesses. According to Rosenberg Research, semiconductor-related companies now account for roughly 18% of the S&P 500’s total market capitalization.

On a relative basis, most other sectors have significantly underperformed. This naturally raises the question: how much further can this momentum continue?

History shows that when one sector becomes heavily favored, opportunities often emerge elsewhere. Areas that have been overlooked frequently begin to offer more attractive valuations and stronger long-term entry points. Investors therefore face a familiar choice: continue chasing momentum or gradually position themselves in sectors that may not deliver immediate excitement but offer compelling value over time.

One area we currently find attractive is infrastructure. The sector continues to face short-term headwinds, including higher energy costs and slower project deployment. Nevertheless, substantial infrastructure budgets approved across Europe and North America are gradually moving into implementation, which we believe should increasingly translate into stronger earnings visibility.

Infrastructure also plays an important role in the rapidly growing buildout of data centers. Due to the current geopolitical environment, digital sovereignty has become an increasingly important topic in Europe. The continent plans to significantly expand its data capacity by 2033 to support artificial intelligence and protect critical data infrastructure. Governments and corporations alike are seeking alternatives to an overreliance on large U.S. technology providers such as Microsoft, Google, AWS, and Zoom.

This transition will take time, but it could eventually create the foundation for a new European technology cycle. Many companies developing these alternatives remain privately owned today. As demand grows, the need for capital investment will likely increase, creating incentives for future public listings. In the meantime, we continue to favor businesses that benefit indirectly by helping build the infrastructure these firms require.

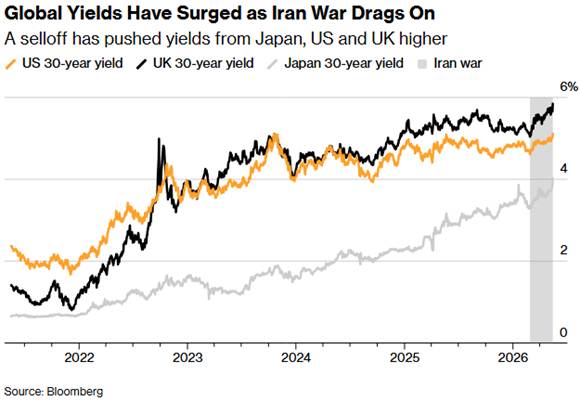

Bond Investors Did Not Get the Memo

While equity markets continue to push higher, bond markets are telling a more cautious story.

Concerns about persistent inflation have led investors to rethink expectations for future interest rate decisions, triggering a sell-off in government bonds. U.S. 30-year Treasury yields recently climbed above 5.10%—levels not seen since 2023. (Source: CNBC)

When bond prices fall, yields rise. Since the fixed interest payment remains unchanged, investors demand lower prices in order to compensate for the risk of higher inflation and higher future interest rates.

The same trend is visible internationally. In the United Kingdom, domestic political uncertainty, with current prime minister Keir Starmer being likely to be replaced by Andy Burnham, pushed 30-year gilt yields to levels last seen in the late 1990s. Investors remain concerned about the possibility of increased public spending and rising debt burdens. Japan faces similar challenges, with long-term bond yields reaching their highest levels since 1999 amid growing concerns about government debt sustainability. [Source: Bloomberg (Paywall)]

If bond investors are correct, several central banks may eventually be forced to maintain higher interest rates for longer than markets currently expect. This would create challenges for highly valued growth-companies, whose valuations depend heavily on future cash flow assumptions and lower discount rates.

This environment once again highlights why discipline in investing matters. Successful long-term investing is rarely about predicting every market move correctly. It is about maintaining balance, managing risk, and rebalancing portfolios when necessary. Many investors believe they can outsmart the market. In reality, consistently doing so is extremely difficult. Remaining more disciplined than the market, however, is achievable.

Green for the Greenback

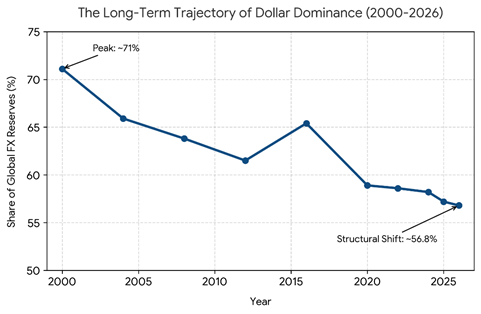

The U.S. dollar has strengthened again recently, leading many to ask why the greenback continues to perform well despite rising debt levels and long-term structural concerns.

History offers part of the answer. During periods of oil shocks and geopolitical uncertainty, the U.S. dollar often strengthens. Higher oil prices fuel inflation fears, which in turn push interest rates higher and attract capital into U.S. government debt markets.

We saw this dynamic during the oil crisis of 1973, when OPEC’s export restrictions caused oil prices to surge dramatically. A similar pattern unfolded in the early 1980s during the Iran-Iraq war, when then-Federal Reserve Chairman Paul Volcker raised interest rates aggressively to combat inflation, ultimately driving substantial dollar strength.

At the same time, investors continue to seek safety in traditional havens such as the Swiss franc and Swiss government debt, even though Swiss yields remain comparatively low.

Still, while short-term periods of U.S. dollar strength are normal, the broader long-term trend remains clear: the dollar’s global dominance is gradually facing increasing challenges. For investors thinking in generational terms, periods of dollar strength should be viewed as opportunities to reassess whether overall currency exposure remains appropriately diversified. (Further reading: IMF Data)

The Unproductive Asset

Warren Buffett was never a fan of precious metals as, in his words, they are an “unproductive asset.” That does not mean no exposure to precious metals at all. In 2020, Berkshire Hathaway surprise markets when they announced that they took a stake in Barrick Gold. (Source: Yahoo Finance)

Since then, a lot of water has flown under the bridge. Precious metals have experienced significant volatility, despite repeated claims that the asset class was “finished.” Gold, silver, and platinum have all delivered substantial gains over recent years. In March 2020, silver traded below USD 15 per ounce. Today, prices remain dramatically higher. (Source: Macrotrends Silver Price History)

Someone once told me that gold itself does not necessarily rise in value—the purchasing power of fiat currencies simply declines over time. Regardless of which perspective one prefers, precious metals have historically played an important role in long-term wealth preservation.

At the same time, investors must remember what “long term” truly means. Investors who bought gold near its peak in 2011 waited almost nine years merely to break even. For silver and platinum investors, the waiting period was even longer.

Why repeat this point? Because even when the long-term outlook appears favorable, markets rarely move in straight lines. While we remain positive on precious metals given recurring inflation pressures, rising debt burdens, and ongoing geopolitical tensions, the path forward may still require patience. It is entirely possible that the next major move upwards takes far longer than many currently expect.

That is why successful investing requires emotional discipline and a clear understanding of time horizons. Markets will always create excitement, fear, optimism, and doubt. Investors who react emotionally to every headline often end up making short-term decisions that hurt long-term outcomes. The most successful wealth preservation strategies are built not around the next quarter or even the next few years, but around generations. Thinking generationally encourages patience, diversification, and resilience. Qualities that have historically mattered far more than trying to predict the next market move.