From Pressure to Opportunity

On August 1st, while Switzerland celebrated its National Day, the U.S. administration delivered a surprise of its own: a 39% tariff on products imported from Switzerland. For many here, the announcement felt like an unnecessary and disproportionate move—especially given that the European Union was granted a far lower rate of 15%. Many had expected that Switzerland, with its long-standing economic ties to the U.S. and its track record as a trusted trade partner, would receive equal or even better treatment.

Yet history reminds us that this is not the first time Switzerland has found itself under external pressure. Over the decades, our small nation has faced its share of political and economic challenges from abroad—often from countries seeking to protect their own industries or to influence Swiss policy. In many cases, such moves have been less about economic necessity and more about frustration or even jealousy over Switzerland’s resilience and prosperity. We have endured banking pressure from the EU, international scrutiny from supranational organizations, and disputes over trade before.

Each time, Switzerland has adapted, emerging stronger and more competitive. Our economy is built on principles that withstand turbulence: innovation, fiscal discipline, a culture of quality, and a deep respect for the rule of law. These qualities have earned Switzerland its reputation as a “diamond” in the global economy—highly valued, rare in its stability, and sought after for its ability to preserve value in a changing world. That is why, even in the face of a 39% tariff, there is little doubt that we will navigate the challenge successfully.

The Unseen Toll on Small Business

Looking across the Atlantic, the immediate reaction in U.S. financial markets has been muted. Major stock indexes remain near record highs, buoyed by strong earnings reports and a wave of investor optimism. For those heavily invested in equities, this is welcome news. But as is often the case, the surface tells only part of the story.

Beneath the upbeat headlines lies a more complex reality. According to the U.S. Chamber of Commerce, there are roughly 236,000 small-business importers in the United States—companies employing fewer than 500 people. Together, these firms brought in over $868 billion worth of goods from abroad in 2023. Unlike large multinationals, smaller companies often lack the resources and flexibility to rapidly reconfigure their supply chains. For them, sudden tariffs can be devastating, eroding profit margins and leaving little room to maneuver.

In both the U.S. and Switzerland, small and mid-sized businesses are the backbone of the economy. In the U.S. alone, they employ some 59 million people—about 46% of the entire private-sector workforce. When such a large segment of the population feels uncertain about its financial future, the effects spread quickly. Consumer spending can slow, sentiment can shift, and the broader economy can feel the chill.

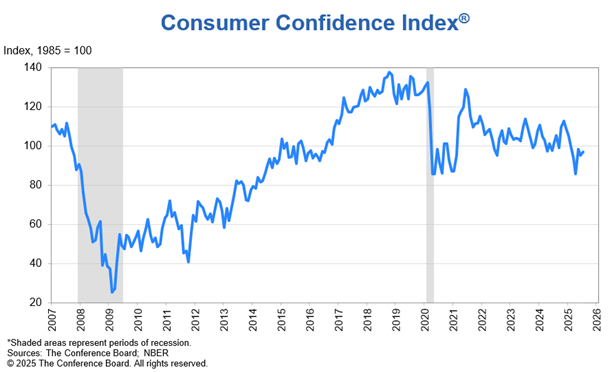

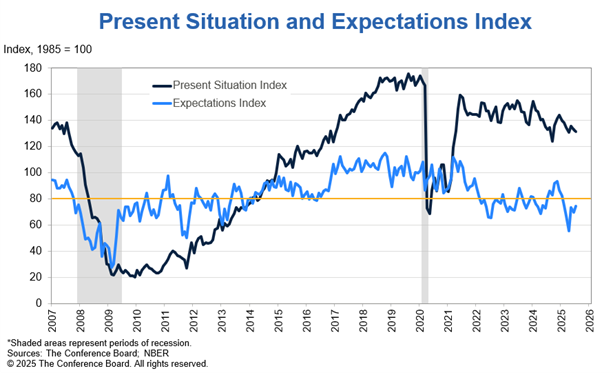

Recent consumer sentiment data in the U.S. paints a nuanced picture. While the Consumer Confidence Index rose in July by two points to 97.2, and the Expectations Index improved to 74.4, the Present Situation Index declined. The Expectations Index remains well below the threshold of 80, which is often seen as an early warning signal of a potential recession. Put simply, optimism about the future has improved slightly, but overall confidence remains fragile.

Switzerland’s Steady Hand—For Now

Meanwhile, the Swiss economy continues to show resilience. Growth remains steady, inflation is under control, and our industries are well-positioned to adapt. The immediate impact of the 39% tariff is likely to be contained. But if the measure remains in place over the long term, it could shave some momentum from GDP growth.

For now, pharmaceuticals—Switzerland’s largest export sector—are exempt. If that changes, the consequences would be more significant. Yet even here, our companies are far from helpless. Many of Switzerland’s leading pharmaceutical firms already operate production facilities in the U.S., giving them the ability to shift parts of their supply chain if necessary. Strategic flexibility is one of the hallmarks of our corporate landscape.

The U.S. Dollar—A Pause Before More Weakness?

Turning to currency markets, the U.S. dollar has managed to stabilize in recent weeks after a difficult start to the year, hovering around the 97 mark. But the underlying pressures that have driven it lower remain in place. Chief among them is the growing political influence over monetary policy.

The president’s open calls for lower interest rates—and the recent replacement of Federal Reserve Board member Adriana Kugler with Stephan Miran—signal a clear preference for a weaker dollar. Miran himself has publicly written about the potential benefits of a softer currency for U.S. trade. The fact that multiple names have been floated as potential successors to Fed Chair Jerome Powell suggests an environment where central bank independence is under scrutiny. Markets take note of such developments, and confidence in the dollar can erode accordingly.

U.S. Treasury Secretary Scott Bessent shares the administration’s preference for lower rates, further reinforcing the policy direction. From our perspective, periods of short-term dollar strength in such an environment may represent windows of opportunity to diversify into other, more stable currencies such as the Swiss franc or the British pound—currencies backed by stronger fiscal discipline and political independence.

Interest Rates—A Global Balancing Act

Interest rates are falling in multiple jurisdictions, and not always for the same reasons. In the U.K., the Bank of England recently cut rates by 25 basis points to 4%, even as inflation ticked up from 3.4% in May to 3.6% in June. This decision was not unanimous, reflecting the difficulty policymakers face in balancing growth concerns against inflationary pressures. Interestingly, despite the rate cut, the British pound gained ground against the dollar, underscoring the dollar’s vulnerability.

In Switzerland, the Swiss National Bank continues to maintain a zero percent interest rate, with inflation at just 0.2% in July. Some observers speculate about the possibility of returning to negative rates if economic conditions deteriorate, but such measures remain a last resort.

For long-term investors, the global trend toward lower rates makes fixed income less attractive on a risk-adjusted basis. In many cases, the yields available do not sufficiently compensate for the risks involved. We continue to see more compelling long-term opportunities in companies with strong fundamentals and reliable dividends, though bouts of market volatility could create selective openings in fixed income as well.

Precious Metals—Catching Their Breath

Over the past 18 months, gold and silver have been in the spotlight, while platinum struggled to keep pace. That changed earlier this summer when platinum surged past USD 1,400 per ounce after months of difficulty breaking the USD 1,000 barrier.

By mid-July, however, all three metals had lost some momentum. The question now is whether they are simply consolidating before another push higher, or whether we have reached the peak for this cycle. Our view leans toward the former. The same forces that have pressured the dollar and cast doubt on the Fed’s independence continue to support precious metals as a store of value.

That said, no market moves in a straight line. Should broader investor sentiment turn, precious metals may experience pullbacks. In our opinion, such corrections are more likely to represent buying opportunities than reasons to sell—particularly for those seeking to hedge against currency depreciation and political uncertainty.

Looking Beyond the Headlines

Taken together, these developments illustrate the importance of looking beyond short-term market moves and headline optimism. Stock indexes at record highs do not always reflect the underlying health of an economy. Political shifts can weaken currencies in ways that are not immediately visible. Tariffs can quietly erode the competitiveness of small businesses and, therefore, the foundation of a successful economy, even as large corporations continue to thrive.

For investors who hold the bulk of their wealth in one currency, one country, or one asset class, these trends carry clear implications. Concentration brings vulnerability. Diversification—across geographies, currencies, and sectors—is one of the most effective ways to reduce those vulnerabilities.

Switzerland, with its political stability, strong rule of law, and tradition of financial discretion, offers a compelling platform for such diversification. It is not about abandoning the U.S. economy or predicting its decline. It is about balancing exposure, preserving purchasing power, and positioning for opportunities that arise in other parts of the world.

If you’d like to discuss how WHVP can support your long-term financial strategy, we invite you to schedule a free consultation. Let’s explore how an international perspective can support your peace of mind.