Hope, Venmo, and Trillions: What the U.S. National Debt Says About the Future of Your Wealth

The U.S. government now accepts Venmo. Not for taxes, not for passport renewals—but for donations to help pay off the national debt. It may sound like satire, but it’s real. In early 2025, the Treasury quietly enabled the option to make mobile payments through Venmo and PayPal to its long-running “Gifts to Reduce the Public Debt” program. That means American citizens can now use the same app they use to split dinner bills to chip in against a $36.7 trillion liability.

And they are. In 2024, Americans donated over $2.7 million to the effort. In just the first five months of 2025, another $434,500 came in. The numbers may look generous, until you realize that the national debt is increasing by around $55,000 per second. Venmo limits individual payments to $999,999.99—so you’d need to send a full payment every 18 seconds just to keep pace. If that sounds absurd, it’s because it is. But it also reveals something important: symbolic gestures are being promoted where real structural reform is urgently needed.

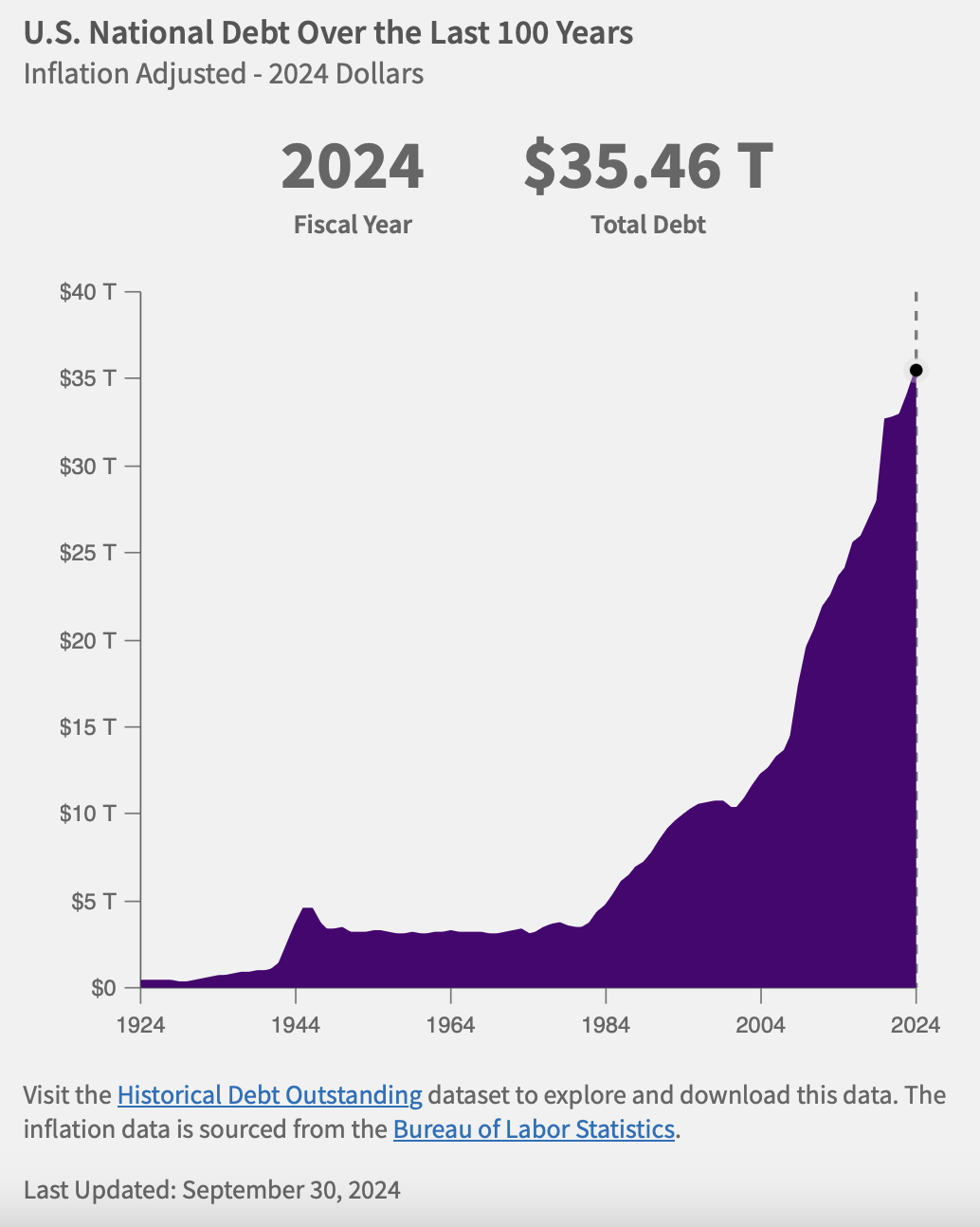

From $5 Trillion to $36 Trillion: A 25-Year Explosion

The debt itself is not new, but the scale is shocking. Just a decade ago, in 2015, the U.S. debt stood at around $18 trillion. In 2000, it was about $5.6 trillion. The fact that it has more than doubled in ten years and increased more than sixfold in 25 years is staggering. And yet, there is little political appetite—on either side of the aisle—to reverse course. Fiscal hawkishness is out, and high-spending populism is in.

Source: US Treasury Fiscal Data

Despite superficial debates about budget ceilings and deficits, neither major party is taking meaningful steps to slow the debt’s growth. In fact, most new legislation—regardless of whether it’s labeled progressive or conservative—seems to come with an ever-higher price tag. The political cost of restraint is too high, and kicking the can down the road has become the standard operating procedure.

Big Bills, Bigger Consequences

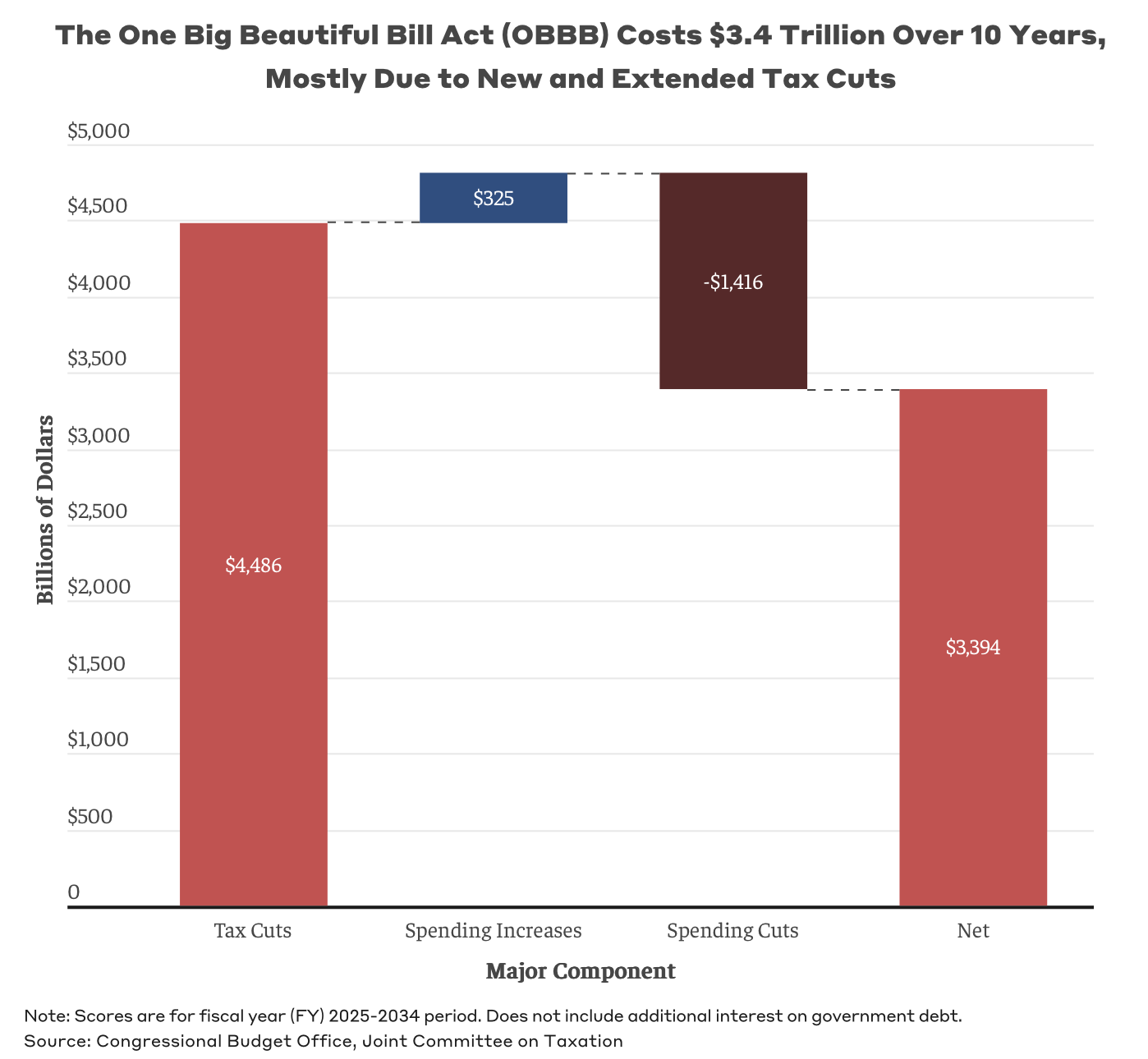

The most recent example is the so-called “Big Beautiful Bill,” signed into law on July 4, 2025. Promoted as a sweeping tax and spending reform, the law permanently extends many of the 2017 Tax Cuts and Jobs Act provisions, adds new tax breaks like zero tax on overtime and expanded deductions for seniors, and only partially offsets its cost with cuts to programs like Medicaid, SNAP, and student loans. According to the Congressional Budget Office (CBO), OBBB will increase the federal deficit by $3.4 trillion over the next 10 years.

Source: Bipartisan Policy

When interest payments on the added debt are included, the total cost rises to more than $4.1 trillion—and potentially $5 trillion if temporary tax breaks are extended, as is often the case in U.S. politics. The law reduces tax revenues by an estimated $4.5 trillion, increases certain spending (especially for defense and immigration enforcement), and only recovers about 25% of the cost through spending cuts. Notably, over 60% of the law’s cost hits in the first five years—suggesting its fiscal impact is heavily frontloaded. In short, OBBB is the most expensive piece of legislation since the 2012 American Taxpayer Relief Act. While framed as relief for working families, the bill reflects the growing tendency of lawmakers to pass massive, debt-financed initiatives with little regard for long-term sustainability. It exemplifies the bipartisan reality: tax cuts are politically popular, spending cuts are painful, and borrowing is the path of least resistance. But that path leads to one place—more debt, and more pressure on the U.S. dollar.

The Quiet Politics of a Weak Dollar

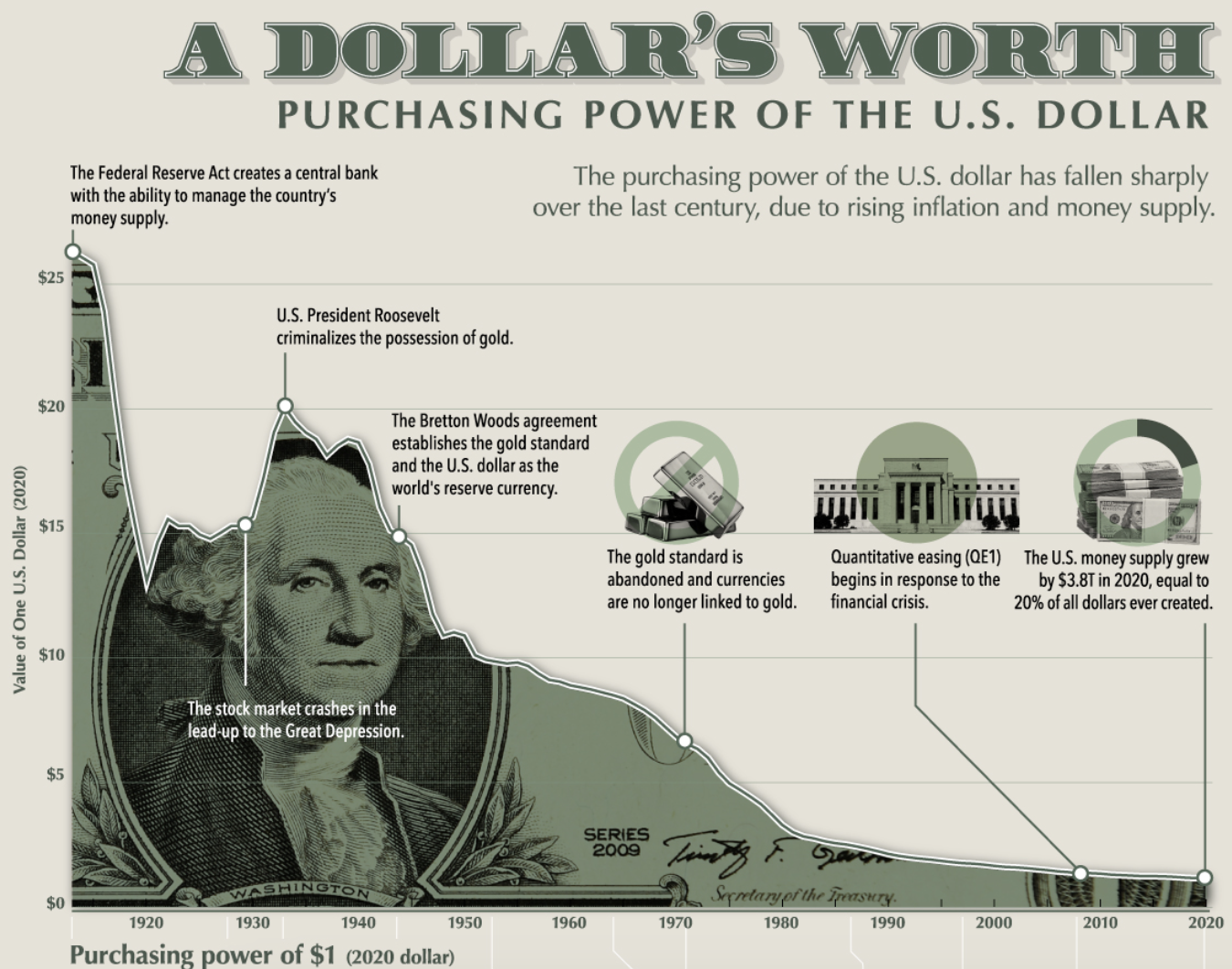

And that brings us to the currency. While American politicians may publicly support a “strong dollar,” the reality tells a different story. The U.S. government has no real interest in maintaining long-term dollar strength. A weaker dollar makes exports more competitive, makes debt payments cheaper in real terms, and reduces the burden of foreign-held U.S. debt. It’s not a coincidence that despite record foreign investment and stock market highs, the dollar continues to face long-term devaluation pressure. Inflation may be moderating in the short term, but the structural forces behind it—namely debt-financed government expansion—remain untouched.

Source: Visual Capitalist

This shift is not accidental. It’s increasingly being formalized in the form of strategic policy initiatives like the Mar-a-Lago Accord, a proposed economic framework under President Trump’s second term. The initiative, still in early-stage development as of 2025, aims to systematically devalue the U.S. dollar while maintaining its status as the global reserve currency—a delicate balancing act designed to resolve the tensions of the Triffin Paradox. By making U.S. exports more competitive and narrowing the trade deficit, the initiative seeks to revive domestic manufacturing and tilt global trade relations in favor of American interests.

Inspired by historical realignments like the 1944 Bretton Woods Agreement and the 1985 Plaza Accord, the Mar-a-Lago Accord envisions a major restructuring of global monetary and trade arrangements. It proposes a mix of tariffs, capital controls, bilateral trade agreements tied to national security, and targeted currency measures to achieve its goals. While much of its content remains classified to avoid disrupting ongoing international negotiations, public statements by key figures like Stephen Miran (Chair of the Council of Economic Advisers) and Scott Bessent (Secretary of the Treasury) have hinted at the Accord’s scope and ambition. Miran’s paper, A User’s Guide to Restructuring the Global Trading System, is seen by many as a conceptual foundation for the plan.

While its long-term success remains uncertain—and while allies and trading partners are watching closely—what’s already clear is that U.S. economic strategy is moving toward a more interventionist and dollar-devaluation-friendly orientation. In this environment, investors must prepare for a future in which the dollar’s purchasing power may erode systematically by design, not just by accident.

Why Investors Should Care

So what does all of this mean for investors, particularly those based in or connected to the United States? It means that relying entirely on U.S.-based assets for wealth preservation may no longer be sufficient. While U.S. markets have shown remarkable resilience, they are not immune to the long-term consequences of fiscal excess and currency erosion.

At WHVP, we specialize in helping American investors diversify internationally—not just to capture new opportunities, but to build financial resilience outside of a system that is increasingly overstretched. Swiss private banking offers a uniquely stable and strategic alternative. Our approach is tailored for long-term capital preservation, privacy, and geopolitical balance. By avoiding direct exposure to the U.S. dollar and markets, we offer a portfolio strategy that acts as a counterweight—not a replacement—to domestic holdings. In our view, this kind of thoughtful diversification is no longer a luxury. It’s a necessity.

The ability to Venmo the government might make headlines, but it won’t solve the real problem. The U.S. national debt isn’t just a number. It’s a reflection of a deeper structural reality—one that investors can no longer afford to ignore.

If you’re ready to take real action instead of symbolic steps, we’re here to help you protect what you’ve built.