Swiss Resilience, U.S. Momentum, and Europe’s Quiet Adjustments

As we move into the final stretch of the year, I find myself reflecting on a period that has been full of contrasts. The third quarter was dominated by strong U.S. markets, pulling global indices along with them. Yet as we now look into the fourth quarter, there is a subtle but noticeable shift: Europe seems to be regaining some energy, Switzerland is defending its competitiveness despite political headwinds, and even the U.S., with all its challenges, has produced news that may still support a year-end rally.

Before diving into the bigger picture, I want to begin with something that genuinely lifted my spirits—some good news for Switzerland that came at just the right moment.

Good News From Switzerland

Many of you will remember the shock earlier this year when President Trump announced a 39% tariff on Swiss goods—revealing the decision on August 1st, our national holiday, of all days. For a country like ours, built on precision, quality, and exports, this felt like a punch to the stomach. But in true Swiss fashion, the government, the business community, and diplomats continued working calmly and diligently behind the scenes.

Their efforts paid off. After a meeting between Swiss business leaders and President Trump, a compromise was reached: the tariff would be lowered from 39% to 15%. Switzerland, in return, will grant additional tariff exceptions on seafood, fish, and certain non-sensitive agricultural products. These adjustments now need parliamentary approval, but we expect a smooth process given how crucial the export sector is for our prosperity.

This outcome is not only a relief—it is a testament to Switzerland’s reputation for reliability and constructive collaboration. For investors, it is an important signal that Swiss companies can continue competing internationally without facing an insurmountable handicap.

A Year-End Rally, Despite High Valuations?

It may sound counterintuitive to expect a rally when markets are already highly valued and geopolitics is as tense as it currently is. But markets often react to momentum shifts rather than perfection—and over the past weeks, the news flow has tilted slightly toward the positive.

One important factor is the improvement in global trade dynamics. Following Switzerland’s agreement, the U.S. administration also decided to remove certain tariffs on goods from Australia, Argentina, Ecuador, Guatemala, and El Salvador. These tariffs had affected everyday items such as beef, bananas, and coffee. These adjustments ease price pressures and help restore healthier trade flows.

Another interesting development has been President Trump’s proposal for a USD 2,000 “tariff rebate check” per person for non-high-income households. While this is not yet finalized, even the idea reflects a desire to cushion the impact of earlier tariff decisions. Should such a rebate be implemented, it would inject additional spending power into the U.S. economy, much like the stimulus checks did during previous cycles.

Finally, after 43 long days, the U.S. government finally ended what has now become the longest government shutdown in history. The agreement reached is valid until January 2026, providing at least temporary stability—though the risk of another shutdown still looms.

Taken together, these developments help explain why we still see a possible year-end rally. But to be clear: the lack of credibility in Washington, along with frequent political reversals, remains one of the biggest risks to such a rally.

Europe: A Mixed Picture with Selective Opportunities

In Europe, the picture remains challenging. Some of the continent’s strongest and historically most reliable economies are struggling to find their footing.

Germany is a good example. Earlier this year, the government announced a EUR 500 billion infrastructure and defense package. An ambitious plan that many hoped would inject much-needed energy into the economy. However, the implementation process has faced numerous obstacles. Experts now expect that less than EUR 100 billion will actually flow into infrastructure and defense, while the rest may end up supporting welfare programs and tax breaks. Unsurprisingly, public patience with Chancellor Merz is fading. His commitment to fiscal discipline during his leadership campaign contrasts sharply with the scale of spending now being discussed.

Across the Channel, the UK is experiencing similar uncertainty. Rachel Reeves had initially promised not to raise taxes, only to later consider increasing income taxes before changing course again. This back-and-forth is unsettling for markets. It also drives up the UK’s financing costs at a time when the country is already spending around 10% of its tax revenue on interest payments. The graph below shows the 10-year government bond yield increase due to the changing course.

Amid all this, it is encouraging to see European companies taking matters into their own hands. Many have begun adjusting their cost structures, streamlining workforces, and improving operational efficiency. These actions, while rarely celebrated in headlines, are often the first steps toward recovery. Investors tend to be forward-looking. When sentiment has been depressed for a long time, even small improvements can spark renewed optimism.

This is why selectivity is essential today. It is not the time to buy broad indices blindly. Instead, the focus should be on identifying companies that can emerge stronger from the current challenges—the winners of tomorrow. This requires patience, an understanding of one’s own risk appetite, and a willingness to invest based on conviction rather than sentiment.

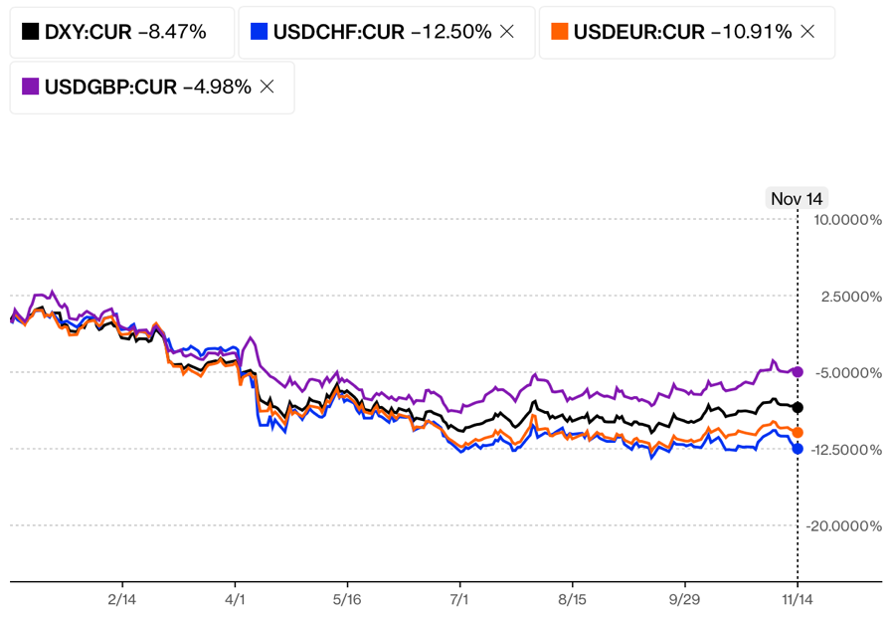

The Swiss Franc: Safe, Steady, and Still Standing Strong

A few weeks ago, I found myself in a lively discussion about which currency is the strongest in the world. With full confidence, I said the Swiss franc. The other person insisted it was the Kuwaiti dinar. As it turns out, a quick consultation with our trusted friends—Google, ChatGPT, and Copilot—proved that the dinar is indeed the strongest in terms of exchange rate.

But that raised an important question: what is the safest currency?

Here, I would still confidently name the Swiss franc, as our previously mentioned sources will confirm.

The Kuwaiti dinar is pegged to the U.S. dollar. If the USD weakens, the KWD weakens with it. The Swiss franc, however, stands entirely on its own. This independence—and the strength of the Swiss economy—has kept the franc resilient, even during periods of high tariffs.

In 2025, the USD index weakened by 8.47%. Against the franc, it was down 12.5%. Interestingly, that decline happened mostly by early July, after which the USD/CHF pair moved sideways. We expect the dollar to gain some temporary strength before continuing its long-term weakening trend. But whatever happens in the short term, it is clear that holding part of one’s wealth in Swiss francs remains a meaningful protective measure. Especially for U.S. investors concerned about the ongoing devaluation of the USD.

And by the way: the dollar also lost more than 12% against the Mexican peso this year, a reminder that global currency dynamics continue to shift in sometimes unexpected ways.

Precious Metals: Time Is Your Friend

Gold reached USD 4,379.13 an ounce in late October before taking a breather. Silver climbed to USD 54.42 before slipping below USD 50 again. These movements always raise the same question: where will they go next?

What gives silver its long-term appeal is its structural supply situation. According to the Silver Institute, 2025 is expected to be the fifth consecutive year of a production deficit. The deficit this year is estimated at 95 million ounces, bringing the total deficit over the last five years to around 820 million ounces.

This is remarkable. Yet as we have seen, prices do not always rise in a straight line. Higher prices encourage innovation—whether through finding substitutes or through entirely new technologies. But silver is exceptionally difficult to replace due to its unique combination of conductivity, reflectivity, and malleability. Its importance in technology, industry, and medicine means demand is unlikely to fade.

At WHVP, we have always treated precious metals as long-term companions. We held them for clients through the challenging years between 2012 and 2018 and continued to buy for those who joined us during that period. Selling this approach was not always easy, but it was the right thing to do for portfolio diversification and long-term security. Not every client needs precious metals, but those who do benefit from our long-term, steady approach—not from “fashion investing.”

Final Thoughts

Despite the uncertainty in global markets and the many challenges still ahead, this environment also presents meaningful opportunities—especially for long-term investors willing to think internationally and protect themselves from currency risks. Our goal at WHVP has always been to help you preserve what you have built and to position your wealth sensibly in a world that is becoming more complex.