The Biggest Risk is to take no Risk at all

What a difference a few weeks can make. The year started on a very strong footing—markets were optimistic, sentiment was positive, and many investors felt reassured about the path ahead. Then reality reminded us, once again, how quickly things can change.

The escalation of the war involving Iran has shown how fragile short-term gains can be. Roughly one month into what was initially expected to be a short intervention, many major indices have slipped into negative territory year-to-date.

Beyond the economic implications, conflicts like these carry a much deeper weight. They bring human suffering on a scale that is difficult to comprehend—families torn apart, lives disrupted, and uncertainty becoming the daily reality for millions. It is important not to lose sight of this human dimension when we speak about markets and investments.

At the same time, history teaches us that while wars affect markets, it is not the events themselves but the uncertainty around them that investors struggle with most.

Stagflation and the Return of Uncertainty

Markets are currently reacting to a complex mix of risks. The conflict involving Israel, Iran, and the United States has widened, with Houthi forces in Yemen adding further tension by threatening key shipping routes in the Red Sea. This raises concerns about global trade disruptions—reminding many of the Suez Canal blockage—and this in addition to the 20% of global oil supply at risk due to the blockage of the Strait of Hormuz.

For investors, the core issue is not only what is happening, but what might happen next.

Central banks themselves are signalling uncertainty. When Federal Reserve Chair Jerome Powell says, “We just don’t know,” it reflects the reality markets are facing. At the same time, he made it clear that without progress on inflation, further rate cuts are unlikely. This places investors in a difficult position, particularly in fixed income markets.

When rising inflation meets slowing economic growth, we enter the territory of stagflation—a challenging environment for almost all asset classes. U.S. GDP growth slowed toward the end of 2025, coming in at 0.7% for Q4, after 4.4% for Q3. While still positive, the trend raises questions. Was this a temporary slowdown, or the beginning of something more persistent?

It is worth noting that government spending declined significantly—by around 16%—which had a meaningful impact on growth figures. Should this reverse, we may well see stronger numbers again. And as expectations shift, so too can markets.

Europe, meanwhile, is not without its challenges. However, one important difference remains: valuations. European markets continue to trade at significantly lower levels compared to the U.S., which provides a degree of downside protection. That said, global risks—from geopolitical tensions to structural issues in private debt, software, and AI-related spending—remain relevant everywhere.

In such an environment, one principle becomes increasingly important: quality.

Being out of the market entirely is rarely a solution. But being selective is. This is one of the key reasons why we do not believe in relying solely on passive investments. Instead, we focus on companies with strong fundamentals, proven resilience, and the ability to navigate changing environments. Businesses that have created value over decades—or even generations—tend to have one key advantage: experience in managing uncertainty.

Interest Rates: Stuck for Now?

Just a few months ago, the outlook for falling interest rates throughout 2026 seemed almost certain. I will admit—I was among those who expected a clearer downward path. Today, the picture is more complex.

Inflation is showing signs of persistence, while growth risks are increasing. This combination brings us back to the concept of stagflation. The question then becomes: how do policymakers respond?

Reducing inflation is difficult. Stimulating growth, on the other hand, is often politically and practically easier—typically through increased government spending. However, this creates its own challenges. High spending combined with elevated interest rates leads to rising debt servicing costs.

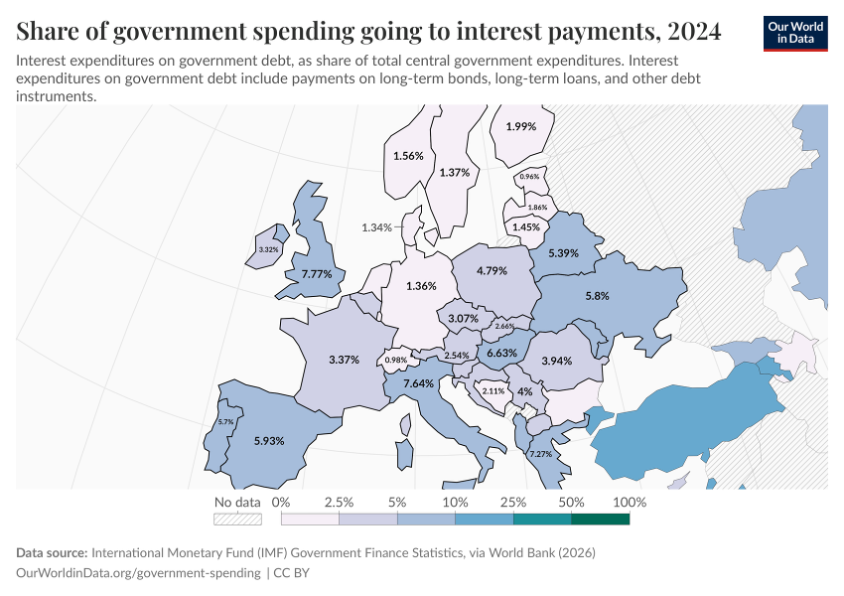

In 2025 alone, the United States spent approximately $1.22 trillion on interest payments—around 14–17% of total federal spending. In Europe, this figure ranges between 1% and 8%, but the direction is similar.

Another consequence is the crowding out of private investment. When governments become dominant borrowers, private investors step back—both because financing becomes more expensive and because government demand often takes priority.

For sustainable growth, fiscal stimulus and lower interest rates ideally go hand in hand. Without that balance, pressure builds within the system.

This dynamic is also visible in bond markets. With interest rate expectations shifting, bond prices have come under pressure—bringing back memories of 2022. For investors holding bonds to maturity, this volatility is often temporary. However, it reinforces the importance of understanding what you own.

This is particularly relevant in areas such as private credit. Many of these investments are structured in ways that make risk difficult to assess. Even when information is available, it is not always easy to interpret. This is not a criticism—it is simply a reality. Complexity does not equal safety. And history has shown us, most notably in 2008, what can happen when complexity meets misplaced confidence.

The USD Paradox

One of the more interesting developments recently has been the temporary strength of the U.S. dollar—despite rising debt, geopolitical involvement, and slowing growth.

Why is that?

In many cases, global portfolios are measured in U.S. dollars. When uncertainty rises, investors often reduce risk and move into cash. And that cash is typically held in USD. In doing so, they preserve nominal performance—even if purchasing power continues to erode over time.

From our perspective, such phases of dollar strength often present opportunities. Opportunities to diversify, to rebalance, and to reduce long-term currency risk.

We remain convinced that the broader trajectory of the U.S. dollar is one of gradual weakening. Structural factors, including rising debt and shifting global dynamics, support this view. The current geopolitical environment may even accelerate the desire of some countries to move away from USD dependency.

In that context, the Swiss franc continues to stand out as a stable and reliable alternative for long-term wealth preservation.

Precious Metals: A Pause, Not a Change in Direction

Precious metals have experienced a pullback after a strong start to the year. Silver, in particular, showed extreme movements—at one point reaching levels that raised more concern than comfort.

It is natural in moments like these to question whether gold still fulfills its role as a hedge. Our answer remains unchanged.

Gold has historically shown a tendency to decline alongside broader markets in the initial phase of a correction. One key reason is liquidity. When leveraged investors face margin calls, they sell what they can—not necessarily what they want. Gold, being liquid, often becomes a source of cash.

However, once this phase passes, gold has repeatedly demonstrated its ability to recover more quickly than broader markets and to provide the stability investors seek.

We therefore view the current development not as a structural shift, but as part of a familiar pattern.

Final Thoughts

If the first quarter has reminded us of anything, it is that markets do not move in straight lines—and that uncertainty is a constant companion in investing. Wars, political shifts, and economic concerns will continue to create volatility. Yet over time, markets have consistently found ways to adjust, adapt, and move forward.

For long-term investors, the key is not to react emotionally to short-term events, but to remain grounded in a well-structured strategy. Diversification across currencies, a focus on quality investments, and a disciplined approach to risk remain as relevant as ever. Periods like this are not a sign to step away, but rather a reminder of why a thoughtful, internationally diversified portfolio matters in the first place.

At WHVP, we continue to monitor developments closely and position portfolios with care and conviction. If anything, environments like the current one reinforce the value of having a stable Swiss foundation within your overall wealth strategy.