The Swiss View: Be Brave, Not Greedy!

While this year indices look great, the economies do not. Investors are falling back into old habits, becoming too enthusiastic about positive signs such as decreasing inflation and ignoring threats such as the looming recession. As many experts, central bankers, and not at least the Bank of International Settlements are stressing, the last bit of the fight against inflation is the most challenging part. Therefore, everyone who thinks that inflation will continue to fall at the same pace as it did since the end of last year is either not showing a great understanding of how economies and monetary policy work or is just naïve. As shown in our previous publication, core inflation is moving very little at a very high level.

We have recently seen that central banks in the developed markets generally have further increased interest rates. An exception is the Federal Reserve in the U.S. and the Bank of Japan, which have paused. However, Jerome Powell had already prepared the markets for more to come. In the United Kingdom, the Bank of England had no choice but to further increase interest rates to deal with high inflation. The same is true for Europe. In Switzerland, the Swiss National Bank has also decided on another interest rate increase of about 0.25%.

While central bankers in developed countries further increase interest rates or announce their plans to continue, central bankers in emerging or frontier markets reduce interest rates to fight slowing growth. One way or another, the signs that led to the decisions are not good.

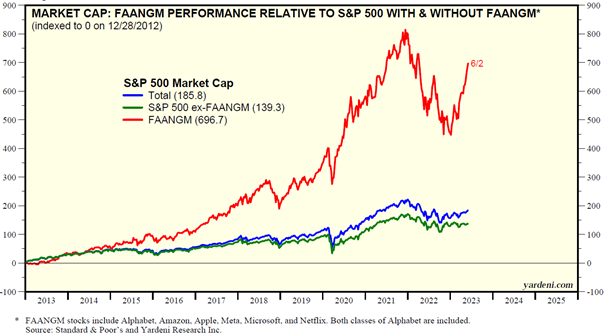

As mentioned above, equity indices have moved up this year so far. This could lead to people suffering from the famous phenomenon of FOMO (fear of missing out) again. However, the indices created by the S&P or Nasdaq say little about how well the economy and the companies, more broadly, are doing. The U.S. market is one of the most extreme examples to show that. Below, you see the difference in the performance of the S&P500 when excluding the FAANGM companies (Facebook (Meta); Amazon; Apple; Netflix; Google (Alphabet); Microsoft). The graph goes back to 2013, which shows, even more impressively, how much of a difference these FAANGM companies contribute to the index’s performance.

It is otiose to talk about how low interest rates were for the last decade. However, it is essential to discuss what the rising interest rates cause in the economies. Last year, we could observe the bond market crashing simultaneously with the equity market. After one of the worst periods, investors were piling into debt earlier this year. Famous banks praised the outstanding performance fixed income will show this year. Six months into the year, the same people realize that, once again, they were wrong. But what caused this misjudgment?

First, inflation rates are coming down, but some need to realize that this is not a linear decrease back to two percent. Additionally, as mentioned above, core inflation is sticky. As you can see, we have the same issue here as with the indices. If you follow headline inflation, you get only part of the picture. I.e., you should be aware of what inflation is built of, the underlying measures, and how they move.

Another mistake was focusing on lagging indicators, such as the unemployment rate. We have criticized that for some time already. There are better ways to go than observing factors that lag economic development. You can lay off your staff within one day in the U.S. In Europe, it is more challenging since we have quite extensive notice periods by law.

Nevertheless, everyone was and still is talking about workforce shortage. In such an environment, you usually do not get rid of your staff where you have a common history and therefore know what to expect. However, when companies enter a period of depressed earnings, it still is one of the easiest ways to save substantial costs. And this is what happens now.

Last but not least, central banks lost their credibility, making investors believe they would not walk their talk. Accordingly, the expectation was that the Fed, in particular, would start loosening interest rates by mid-2023. This is certainly not the case, as was made clear by Jerome Powell and other central bankers in June. We are confident that central banks will not lower interest rates this year, meaning we will see another Paul Volker rather than Arthur Burns. Central Banks move on thin ice and must be careful not to lose their credibility entirely.

Remember, our last publication had the title "Cash is King." There, we shared the importance of having enough cash on hand and ensuring that when entering an investment, the company should generate enough money to cover all its interest payments, reduce debt, and pay dividends. We stay with this statement and stress having enough cash for new investments.

However, being confronted with an inflation rate of four percent or above, the question is which currency to choose. In this matter, I emphasize the importance of not being impatient and not being focused too much on the short-term success of your investment strategy. You may be unable to beat high-running inflation in the short run. Therefore, focus on your portfolio's long-term success since inflation will not stay high forever.

In the meantime, we focus on currencies issued by economies with a stable debt-to-GDP (gross domestic product) ratio or those that have lost so much value recently that the currency simply is oversold. Furthermore, due to the energy transformation and the infrastructure programs around the globe, currencies from commodity-rich countries bear the potential to strengthen in the long term.

Considering the expected volatility within the second half of this year, safe haven currencies would be an attractive place to park your cash, collecting some interest in the meantime.

As we stressed in May, the expected in-between correction in precious metals has started. From its high, gold corrected by about seven percent while silver has corrected by about 14%. We are not totally convinced that the in-between correction is over yet. Having said that, since our crystal ball is no clearer than anybody else's, we believe that it would be reasonable to start building up a position in precious metals at the current levels. If you already have precious metals in your portfolio, deciding whether it is the right time to increase your exposure to precious metals depends on your overall asset allocation and preferences.

Having said that, we again believe that we find ourselves in a bear-market rally. Accordingly, the latest ride up the hills will be followed by a ride down into another valley. Warren Buffet once said:

Once that happens, our job is to be ready to pick the right fruits in the universe of investment opportunities.

We have recently seen that central banks in the developed markets generally have further increased interest rates. An exception is the Federal Reserve in the U.S. and the Bank of Japan, which have paused. However, Jerome Powell had already prepared the markets for more to come. In the United Kingdom, the Bank of England had no choice but to further increase interest rates to deal with high inflation. The same is true for Europe. In Switzerland, the Swiss National Bank has also decided on another interest rate increase of about 0.25%.

| Interest rate hike June 2023 | Current interest rate | Inflation rate May 2023 (year-on-year) | |

| Federal Reserve (USA) | 0% | 5.25% | 4% |

| Bank of England (GB) | 0.5% | 5% | 8.7% |

| European Central Bank (EU) | 0.25% | 3.5% | 6.1% |

| Bank of Japan (JP) | 0% | -0.1% | 3.2% |

| Swiss National Bank (CH) | 0.25% | 1.75% | 2.2% |

| State Bank of Vietnam (VD) | -0.5% | 4.5% | 2.43% |

| People’s Bank of China (CN) | -0.1% | 2.65% | 0.2% |

While central bankers in developed countries further increase interest rates or announce their plans to continue, central bankers in emerging or frontier markets reduce interest rates to fight slowing growth. One way or another, the signs that led to the decisions are not good.

Do not Burn your Fingers due to Eagerness

As mentioned above, equity indices have moved up this year so far. This could lead to people suffering from the famous phenomenon of FOMO (fear of missing out) again. However, the indices created by the S&P or Nasdaq say little about how well the economy and the companies, more broadly, are doing. The U.S. market is one of the most extreme examples to show that. Below, you see the difference in the performance of the S&P500 when excluding the FAANGM companies (Facebook (Meta); Amazon; Apple; Netflix; Google (Alphabet); Microsoft). The graph goes back to 2013, which shows, even more impressively, how much of a difference these FAANGM companies contribute to the index’s performance.

Too Low for too Long

It is otiose to talk about how low interest rates were for the last decade. However, it is essential to discuss what the rising interest rates cause in the economies. Last year, we could observe the bond market crashing simultaneously with the equity market. After one of the worst periods, investors were piling into debt earlier this year. Famous banks praised the outstanding performance fixed income will show this year. Six months into the year, the same people realize that, once again, they were wrong. But what caused this misjudgment?

First, inflation rates are coming down, but some need to realize that this is not a linear decrease back to two percent. Additionally, as mentioned above, core inflation is sticky. As you can see, we have the same issue here as with the indices. If you follow headline inflation, you get only part of the picture. I.e., you should be aware of what inflation is built of, the underlying measures, and how they move.

Another mistake was focusing on lagging indicators, such as the unemployment rate. We have criticized that for some time already. There are better ways to go than observing factors that lag economic development. You can lay off your staff within one day in the U.S. In Europe, it is more challenging since we have quite extensive notice periods by law.

Nevertheless, everyone was and still is talking about workforce shortage. In such an environment, you usually do not get rid of your staff where you have a common history and therefore know what to expect. However, when companies enter a period of depressed earnings, it still is one of the easiest ways to save substantial costs. And this is what happens now.

Last but not least, central banks lost their credibility, making investors believe they would not walk their talk. Accordingly, the expectation was that the Fed, in particular, would start loosening interest rates by mid-2023. This is certainly not the case, as was made clear by Jerome Powell and other central bankers in June. We are confident that central banks will not lower interest rates this year, meaning we will see another Paul Volker rather than Arthur Burns. Central Banks move on thin ice and must be careful not to lose their credibility entirely.

Currency Diversification

Remember, our last publication had the title "Cash is King." There, we shared the importance of having enough cash on hand and ensuring that when entering an investment, the company should generate enough money to cover all its interest payments, reduce debt, and pay dividends. We stay with this statement and stress having enough cash for new investments.

However, being confronted with an inflation rate of four percent or above, the question is which currency to choose. In this matter, I emphasize the importance of not being impatient and not being focused too much on the short-term success of your investment strategy. You may be unable to beat high-running inflation in the short run. Therefore, focus on your portfolio's long-term success since inflation will not stay high forever.

In the meantime, we focus on currencies issued by economies with a stable debt-to-GDP (gross domestic product) ratio or those that have lost so much value recently that the currency simply is oversold. Furthermore, due to the energy transformation and the infrastructure programs around the globe, currencies from commodity-rich countries bear the potential to strengthen in the long term.

Considering the expected volatility within the second half of this year, safe haven currencies would be an attractive place to park your cash, collecting some interest in the meantime.

Here we are… our in-between Correction

As we stressed in May, the expected in-between correction in precious metals has started. From its high, gold corrected by about seven percent while silver has corrected by about 14%. We are not totally convinced that the in-between correction is over yet. Having said that, since our crystal ball is no clearer than anybody else's, we believe that it would be reasonable to start building up a position in precious metals at the current levels. If you already have precious metals in your portfolio, deciding whether it is the right time to increase your exposure to precious metals depends on your overall asset allocation and preferences.

Brave & Greedy…

Having said that, we again believe that we find ourselves in a bear-market rally. Accordingly, the latest ride up the hills will be followed by a ride down into another valley. Warren Buffet once said:

"Be fearful when others are greedy, and be greedy when others are fearful."It seems to us that in the first half of the year, investors were greedy but realized that they might have been too optimistic after all. Should our evaluation of the markets prove correct, there will soon be a time when fear will control the markets again.

Once that happens, our job is to be ready to pick the right fruits in the universe of investment opportunities.