The USD Is Hot… Just Like Summer

The United States once again lived up to the saying that bigger is better. On June 12, SpaceX completed what became the largest IPO in history. With a market capitalization of approximately USD 1.78 trillion and a price-to-sales ratio of around 103, investors are placing an extraordinary bet on the future.

Much of today's valuation is driven by expectations rather than current earnings. Mars colonization, lunar and asteroid mining, commercial space travel—these ideas capture Elon Musk’s dream. Whether they ultimately justify today's valuation remains to be seen. Investors remember that Tesla faced years of skepticism before creating substantial wealth for many shareholders. As a result, there is considerable confidence in Musk's ability to turn ambitious visions into reality.

Whether future IPOs, such as OpenAI or Anthropic, will generate the same level of enthusiasm remains uncertain. Markets often become crowded around the most popular stories. Sometimes the better opportunities can be found by looking where fewer investors are paying attention.

Before turning to the markets, we would also like to congratulate Switzerland on reaching the next round of the World Cup, where they will face Algeria this Friday in Vancouver. We also wish Team USA the very best of luck in tomorrow's match against Bosnia and Herzegovina in San Francisco.

Finding Value in Value Investing

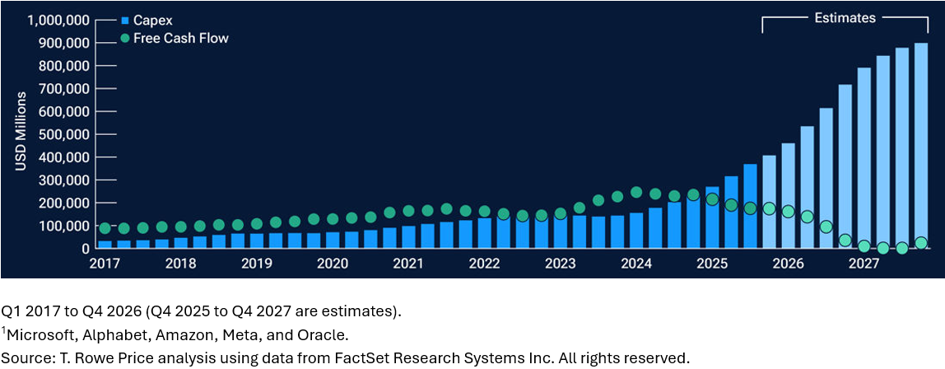

After some weakness in the technology sector during the first quarter, the Artificial Intelligence (AI) investment theme regained momentum at the beginning of the second quarter. At the same time, investors are becoming increasingly aware of the risks that accompany companies trading at very high valuations.

The challenge with many AI companies is that today's share prices are largely based on expectations of future earnings rather than profits being generated today. Investors are betting that the leading companies will continue to outpace competitors and eventually justify these valuations.

The Bank for International Settlements (BIS), in its Annual Economic Report 2026, recently highlighted concerns regarding the sustainability of some AI-related investments. These concerns are not entirely new. Last year, for example, Oracle announced a USD 40 billion order for Nvidia chips, much of it financed with debt, to build data centers that would subsequently be leased to OpenAI for fifteen years. Meanwhile, OpenAI reported an operational loss exceeding USD 20 billion during 2025.

None of this means AI will fail. It simply illustrates that many investments in the sector rely on optimistic assumptions while capital expenditures continue to accelerate.

Institutional investors have gradually started adjusting their portfolios, allocating more capital toward value-oriented investments. While technology companies have significantly outperformed over recent years, many sectors of the real economy have lagged. Infrastructure is one example. These areas may not receive the same headlines, but they can present attractive long-term opportunities.

For long-term investors, diversification should extend beyond asset classes. It should also include different investment styles. Momentum investing can produce excellent returns during certain market environments but combining it with value investing and countercyclical opportunities creates a more balanced portfolio. Industries temporarily overlooked by the market can often provide attractive long-term value, particularly during periods of persistent inflation, higher interest rates, and increasing geopolitical fragmentation.

Although we do not expect inflation to accelerate significantly from current levels, we continue to believe that inflation will likely remain sticky for some time.

The USD Is Hot

Speaking of inflation, U.S. consumer prices increased by 4.2% year-over-year in May, following 3.8% in April. While inflation may moderate somewhat during the coming months, it is likely to remain well above the Federal Reserve's 2% target. In fact, inflation has consistently not been at the Fed's target since early 2021.

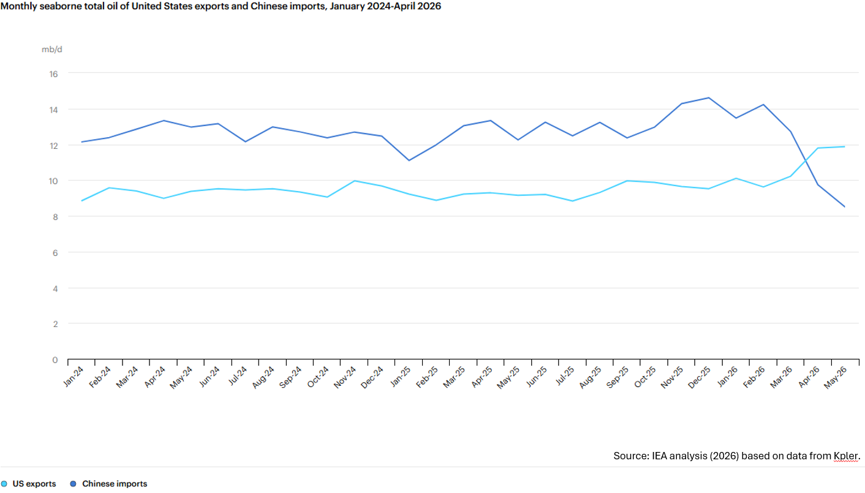

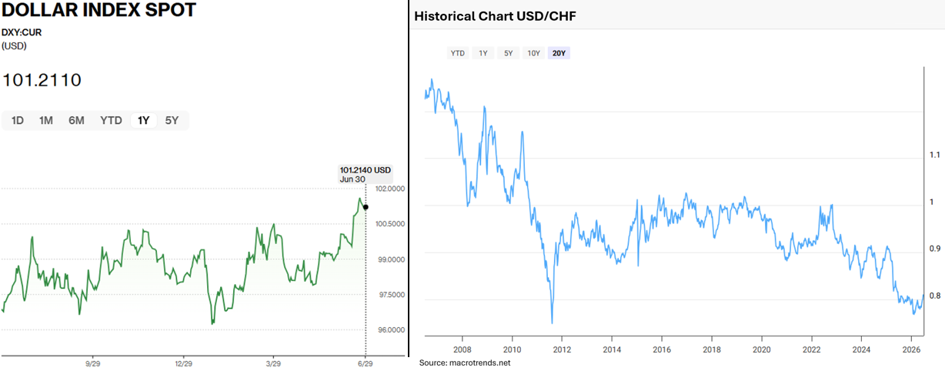

The recent strength of the U.S. dollar is largely supported by expectations that interest rates could remain higher for longer. At the same time, developments in global energy markets have strengthened the dollar further. Following the disruption of shipping through the Strait of Hormuz, the United States has reinforced its position as one of the world's largest oil producers and exporters (How global oil supplies have readjusted to help fill the huge gap left by the Strait of Hormuz shock – Analysis - IEA). Research increasingly suggests that since the U.S. became a net energy exporter, higher oil prices have tended to support a stronger U.S. dollar (The link between oil prices and the US dollar: evidence and economic implications).

The question investors ask is what would eventually lead the dollar to resume its longer-term weakening trend.

At WHVP, we continue to believe that the long-term direction of the U.S. dollar remains downward, particularly against structurally strong currencies such as the Swiss franc. That does not mean the path will be straight. Currency markets move in cycles, and periods of dollar strength are part of that journey.

For U.S. investors holding internationally diversified portfolios, a stronger dollar can temporarily reduce returns when measured in dollars. On the other hand, it also creates attractive opportunities to diversify additional assets internationally at more favorable exchange rates. Long-term investors should view currency movements within the broader context of preserving purchasing power over decades rather than months.

Interestingly, despite a strong U.S. dollar and robust American energy exports, inflation in Europe remains considerably lower. Consumer prices in the European Union increased by 3.3% year-over-year in May, while Switzerland continues to enjoy remarkable price stability with inflation of just 0.6%, comfortably within the Swiss National Bank's target range.

Stable Cash Flow with Limited Risk

Investors seeking stable income often turn to fixed-income investments. High-quality bonds can provide dependable cash flow while generally carrying lower risk than equities. However, higher safety usually comes with lower yields.

It is also important to remember that bond prices fluctuate as interest rate expectations change. When investors expect central banks to raise rates, newly issued bonds become more attractive, causing existing bond prices to decline.

Government bonds have traditionally been viewed as the safest form of debt. However, growing government deficits and rising debt levels have caused many investors to reassess that assumption. Fiscal discipline is becoming increasingly important when evaluating sovereign debt.

For this reason, WHVP generally favors high-quality corporate bonds issued by financially strong companies with healthy balance sheets. Another attractive area includes bonds issued by supranational organizations. Because these institutions are backed by multiple member states, they often benefit from diversified credit support while providing attractive risk characteristics.

Back to 2011?

After an exceptional 2025 and a strong start to 2026, gold and silver have recently experienced a period of consolidation. For some investors, this brings back memories of 2011, when precious metals reached record highs before entering a prolonged correction.

We believe today's environment is fundamentally different.

History rarely repeats itself exactly—it often rhymes. In 2011, central banks flooded financial markets with liquidity while maintaining historically low interest rates. Although consumer inflation remained subdued, asset prices rose significantly across equities and real estate.

Today's backdrop is very different. Inflation remains elevated, geopolitical uncertainty continues to increase, and cooperation between major economies has become more challenging. In our view, the recent pullback in precious metals is more likely a pause than the end of the longer-term trend.

As always, successful investing comes down to proper allocation rather than concentrating on a single opportunity.

Investing Across Generations

Perhaps the greatest strength an investor can have is patience. Financial markets will always experience periods of excitement, greed, uncertainty, optimism, and fear. Making investment decisions based on emotions often leads investors to buy when prices are high and sell when prices are low.

At WHVP, we encourage clients to focus on their long-term objectives rather than short-term headlines. Successfully building wealth and preserving wealth is measured over decades—not quarters. By thinking in generations instead of the next few years, families are better positioned to preserve purchasing power, navigate market cycles, and pass on lasting financial security. Remaining disciplined, diversified, and patient has historically rewarded investors far more consistently than trying to predict every market movement.

This content is for informational purposes only and does not constitute investment, tax, or legal advice. All views reflect our opinions as of the date of publication and may change without notice. WHVP AG is regulated in Switzerland by FINMA and is an SEC-registered investment adviser.