What One Chart Tells Us About the US Economy

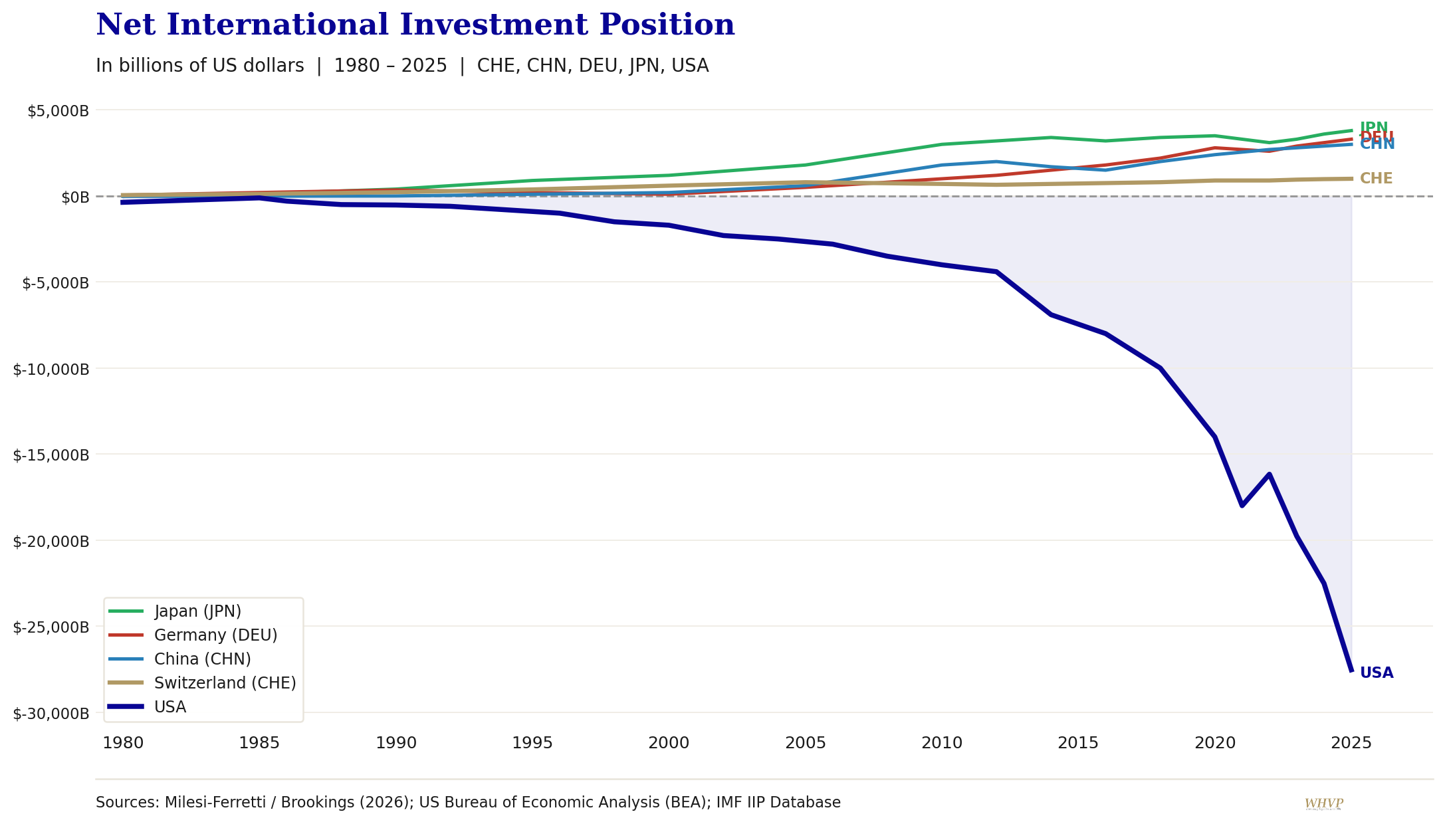

A single chart has been making the rounds in financial circles. It tracks the Net International Investment Position (NIIP) of several major economies from 1980 to today.

One line stands out sharply from the rest: the United States.

For American investors holding or considering assets abroad, understanding what this chart shows, and what it does not show, is worth a few minutes of reflection. It is not a prediction of crisis. It is not a political statement. It is a structural data point that helps explain how the U.S. economy has changed over the past four decades, and why international diversification remains relevant for long-term wealth planning.

What is the NIIP?

The Net International Investment Position measures the difference between a country’s foreign financial assets and its foreign financial liabilities.

In simple terms, it answers the question: does a country own more abroad than foreigners own within it, or the other way around?

A positive NIIP means a country is a net creditor. Its residents, companies, government, and institutions own more foreign assets than foreign investors own in that country.

A negative NIIP means the opposite. Foreign investors own more assets in that country than the country owns abroad.

These assets and liabilities can include government bonds, corporate bonds, equities, direct investments, real estate, banking claims, reserve assets, and other financial holdings. In that sense, the NIIP acts like a national balance sheet between one country and the rest of the world.

Switzerland, Japan, and China all sit in positive territory. The United States does not.

How did the US get here?

In 1980, the United States was the world’s largest creditor nation. Its net international investment position was positive, and the U.S. owned more abroad than foreign investors owned in the United States.

That position changed during the 1980s. In 1986, the United States became a net debtor nation for the first time since 1914. Since then, the country’s NIIP has moved deeper into negative territory.

By the end of 2020, the U.S. net international investment position stood at approximately negative $14 trillion. By the end of 2022, it had reached around negative $16 trillion. More recent data places the figure far lower still, with the gap now measured in the tens of trillions.

According to the U.S. Bureau of Economic Analysis, by the end of the fourth quarter of 2025, the U.S. net international investment position stood at approximately negative $27.54 trillion. That number represents the gap between U.S.-owned foreign assets and foreign-owned U.S. liabilities.

Put differently, foreign investors now own significantly more U.S. assets than Americans own abroad.

Why does this matter for American investors?

This is not a political question, and it is not a prediction. It is a structural data point that long-term investors should be aware of.

When a country runs a persistently negative NIIP, it means a growing share of its assets, its companies, its real estate, its government debt, is owned by foreign investors. The country becomes more dependent on continued foreign investment to fund its consumption and government spending.

For individual investors, this raises a practical question: how much of your wealth is concentrated in one country's financial system, and what would happen to that wealth if confidence in that system shifted?

This is not a hypothetical that requires a crisis to be relevant. It is a standard consideration in long-term wealth planning, and one that Swiss private banking has been built around for decades.

A negative NIIP is not automatically a crisis

It is important to be precise here.

A negative NIIP does not mean a country is bankrupt. It does not mean foreign investors are about to abandon U.S. markets. It also does not mean the U.S. economy is weak.

In fact, part of the reason the United States has such a large negative NIIP is because global investors continue to want exposure to U.S. assets. The U.S. dollar remains the world’s dominant reserve currency. U.S. capital markets are deep and liquid. U.S. companies, especially in technology and innovation, remain among the most widely held in the world.

In other words, a large negative NIIP can reflect confidence in U.S. markets.

But that is only one side of the story.

The other side is dependency. When a country relies heavily on foreign capital to fund its deficits, support its asset markets, and absorb its liabilities, it becomes more exposed to shifts in global confidence. That does not mean confidence will suddenly disappear. It does mean that the system depends on the continued willingness of foreign investors to hold U.S. assets at large scale.

For long-term investors, that is worth understanding.

What does this have to do with the U.S. economy?

The NIIP is closely connected to broader structural trends: trade deficits, government borrowing, currency demand, capital flows, and foreign appetite for U.S. financial assets.

For many years, the United States has consumed and invested more than it has saved domestically. The difference has been financed, in part, by foreign capital. Foreign investors buy U.S. Treasuries, U.S. equities, U.S. corporate bonds, real estate, and direct investments. These inflows help fund deficits and support asset prices.

This relationship has worked for a long time because the United States occupies a unique position in the global financial system. The dollar’s reserve currency status gives the U.S. an advantage that most countries do not have. It allows the country to attract capital on a scale that would be difficult for others to sustain.

However, no structural advantage should be mistaken for a permanent law of nature.

Reserve currency status, market leadership, and investor confidence are powerful. But they are also maintained over time through policy credibility, institutional strength, fiscal discipline, and trust. If any of those weaken, the risks do not necessarily appear overnight. They may build gradually.

That is why the NIIP matters. It is not a short-term market signal. It is a long-term balance sheet indicator.

Why this matters for American investors

For individual investors, the key question is not whether the United States is “good” or “bad.” That framing is too simplistic.

The better question is this:

How much of your wealth is tied to one country, one currency, one banking system, one legal system, and one policy environment?

Many American investors are more concentrated than they realize. Their home, employment income, retirement accounts, bank accounts, brokerage accounts, business interests, and currency exposure may all be tied to the United States.

That concentration can feel normal because it is familiar. But familiarity is not the same as diversification.

If an investor holds most of their assets in U.S. dollars, U.S. institutions, U.S. markets, and U.S. custody structures, they are making an implicit bet that the U.S. financial system will continue to serve their long-term goals better than any alternative combination of jurisdictions.

That may be appropriate for some investors. But it should be a conscious decision, not an accidental default.

What international diversification actually means

International diversification does not mean abandoning the United States.

It does not mean betting against the dollar. It does not mean assuming that a crisis is around the corner. It also does not mean moving assets offshore for secrecy or tax avoidance.

For U.S. persons, any international structure must be transparent, compliant, and properly reported.

At its best, international diversification means building a wealth structure that is not entirely dependent on one country’s financial system. It can include exposure to multiple currencies, multiple markets, multiple custodians, and multiple jurisdictions.

This can help investors think more clearly about questions such as:

How much of my wealth is exposed to the U.S. dollar?

How much is held within the U.S. banking and brokerage system?

How would my portfolio be affected by changes in U.S. fiscal, monetary, or tax policy?

Would holding part of my wealth abroad improve my overall resilience and flexibility?

Am I properly coordinating my investment strategy with my tax, legal, and estate planning obligations?

These are not panic questions. They are planning questions.

Why Switzerland enters the conversation

Switzerland has maintained a positive NIIP for decades. It is a small country, but it plays an outsized role in global wealth management because of its political stability, strong currency, regulatory framework, and long-standing culture of private banking.

For Americans, the appeal of Switzerland is not about escaping the U.S. system. It is about adding a second, well-regulated jurisdiction to a broader financial plan.

A Swiss custody relationship can allow investors to hold assets outside the United States while still maintaining transparency and compliance with U.S. reporting obligations. This can create geographic, currency, and custodian diversification.

That distinction matters.

The value of a Swiss account is not simply the account itself. It is the structure around it: the custodian bank, the independent wealth manager, the reporting process, the investment strategy, and the coordination with U.S. tax and legal advisers.

Switzerland’s financial system is regulated by FINMA, the Swiss Financial Market Supervisory Authority. Independent wealth managers must operate within a defined regulatory framework. For U.S. clients, working with an SEC-registered Swiss adviser can also help bridge the gap between Swiss custody and U.S. investor requirements.

What a Swiss structure can and cannot do

A Swiss account can help create international diversification. It can provide access to a different custody environment. It can support currency diversification. It can help families think beyond a single domestic system.

But it is not a magic shield.

It does not remove U.S. tax obligations. It does not eliminate investment risk. It does not guarantee better performance. It does not make assets immune from market volatility, regulatory change, or reporting requirements.

This is why the structure has to be built properly.

For American investors, the practical questions include:

Which Swiss banks accept U.S. clients?

How are the assets reported?

What role does the wealth manager play?

Who has trading authority?

Who has withdrawal authority?

How are fees disclosed?

How does the account fit into the client’s broader U.S. tax, estate, and investment planning?

These are the details that matter more than slogans about “offshore banking.”

The bigger lesson from the chart

The NIIP chart is not telling investors to make dramatic decisions. It is not telling investors to leave the U.S. market. It is not even saying that the U.S. is in immediate trouble.

What it does show is that the U.S. financial position relative to the rest of the world has changed significantly over the past four decades.

The country that was once the world’s largest creditor has become the world’s largest debtor. At the same time, American households and investors remain heavily concentrated in U.S. assets, U.S. institutions, and the U.S. dollar.

For long-term investors, that combination deserves attention.

Wealth planning is not only about chasing returns. It is also about understanding where assets are held, which systems they depend on, and how resilient the overall structure is across different market and policy environments.

Final thoughts

A single chart will never tell the whole story of an economy. But it can reveal a trend that is easy to overlook.

The United States remains one of the most important financial markets in the world. It continues to offer innovation, liquidity, and investment opportunities that global investors actively seek.

At the same time, the country’s negative NIIP highlights a long-term structural reality: the U.S. depends heavily on foreign capital, and many American investors remain concentrated in the same system that those foreign investors are financing.

International diversification is not about fear. It is about perspective.

For investors with significant wealth, cross-border lives, or long-term family planning needs, holding part of a portfolio in a regulated jurisdiction such as Switzerland may be worth considering as part of a broader, compliant wealth strategy.

WHVP works with American clients who want to understand what this kind of structure looks like in practice, how Swiss accounts work, what the reporting requirements are for U.S. persons, and how international diversification can fit into a long-term wealth plan.

This content is for informational purposes only and does not constitute investment advice or an offer to buy or sell any security. Investing involves risks, including possible loss of principal. WHVP AG is regulated in Switzerland by FINMA and is an SEC-registered investment adviser.

This content is for informational purposes only and does not constitute investment advice or an offer to buy or sell any security. Investing involves risks, including possible loss of principal. WHVP AG is regulated in Switzerland by FINMA and is an SEC-registered investment adviser.

Sources

- US Bureau of Economic Analysis (BEA) — US NIIP data, Q4 2025

- Milesi-Ferretti, Gian Maria — Brookings Institution, External Wealth of Nations Database (2026)

- Net International Investment Position — Wikipedia

- Reuters — U.S. net international investment position reporting

- FINMA — Swiss financial market supervision information

Schedule a free consultation today to explore how international diversification can strengthen your financial future.