When the Music Stops

One thing that stood out to us in 2025 is how much more seriously Americans have started to take the protection of their wealth. The growing eagerness to find safety is not surprising. The U.S. is once again staring down the possibility of a government shutdown, foreign and domestic demand for Treasuries is weakening, and the national debt has now reached USD 37 trillion as of August 2025. Against this backdrop, it becomes clear that relying exclusively on the U.S. market is not so much a strategy as it is the neglect of reality.

Now, that does not mean the rest of the world is free of problems. Far from it. Global government debt hit yet another all-time high in 2024, climbing to USD 102 trillion. And that figure is already adjusted into U.S. dollar terms, despite the dollar strengthening by 7.4% during that same year. On top of that, the wars in both Europe and the Middle East continue with no real prospect of an end.

And yet—Markets Reach New All-Time Highs

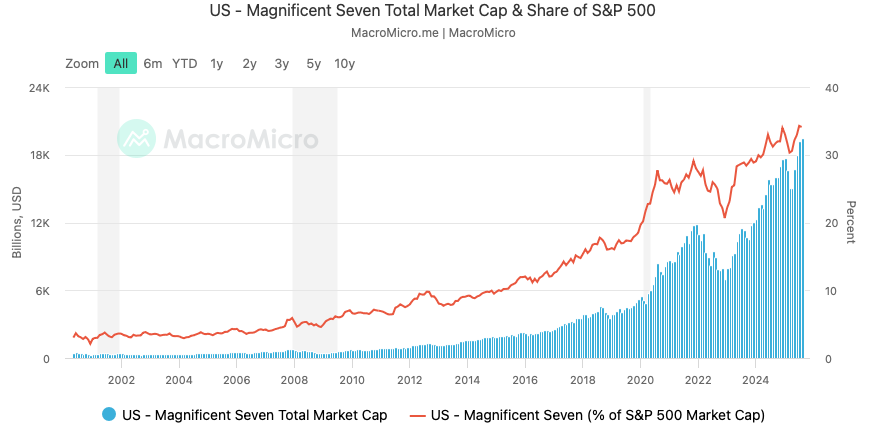

This contradiction has almost become routine. Indices tell one story of wealth and prosperity, while the real economy tells another. I sometimes tire of pointing out this dispersion, but it remains necessary because the gap keeps widening. Stock indices long ago stopped being a reliable indicator of economic wellbeing. Today, fewer than 10% of the companies in some of the main indices account for nearly half the market capitalization and drive performance almost single-handedly. That is not healthy. It is concentration risk of the highest order. And, as everyone should know, what goes up quickly can also come down quickly.

That is why more and more experts are returning to a truth that should never have been forgotten: active and true diversification are essential. In every market, even one that looks broadly expensive, there are always opportunities. Cycles do not move in lockstep across industries. When technology looks overstretched, energy may be underpriced. When growth stocks soar, mining companies may lag behind, and then suddenly catch up.

We have seen this most clearly in the mining industry over the past 18 months. Gold and silver miners disappointed investors for years, even while the gold price itself rose. Many experts agreed that the sector was undervalued, but that undervaluation dragged on for much longer than expected. Then, almost overnight, the rally began—and once it started, it took off like a rocket. Suddenly, the asset class everyone had written off became the star performer.

But here lies the challenge: once a stock has tripled, do you still have the courage to buy it? What was a value trade quickly becomes a momentum trade. At that point, discipline becomes more important than conviction. The lesson is simple: once the crowd joins a trade, it is usually time to start scouting for the next opportunity. And perhaps even more importantly: every investor needs an exit plan. That does not mean liquidating everything, but it does mean harvesting some profits and redeploying those funds into other areas where seeds can grow for the next cycle.

The Quiet Warning in Lower Rates

The contradiction between booming stock markets and weak fundamentals is also visible in the behavior of central banks. If economies were truly as strong as the equity indices suggest, why would central banks everywhere feel the need to lower interest rates? And yet that is exactly what we have seen in 2025. Every major Western central bank has cut rates this year. The Federal Reserve, after much hesitation, finally gave in earlier this month and lowered rates by another 0.25%, indicating more to come. The European Central Bank (ECB) continues its balancing act, trying to serve countries as different as Germany and Greece with a single policy. The Swiss National Bank has already reached zero and is trying to avoid being forced into negative rates once again. Only the Bank of Japan is standing tight and talks about moving in the opposite direction.

Of course, every central bank frames its actions differently. But the underlying reason is always the same: to support and protect the domestic economy. Switzerland, for example, is especially wary of an overly strong franc, which would make life difficult for exporters. The ECB is juggling too many member states with too many needs. The Fed is caught between its dual mandate of stable prices and maximum employment—while also facing political pressure. Stephen Miran, who recently joined the Fed’s Board of Governors, is one of the voices explicitly pushing for lower rates and a weaker dollar.

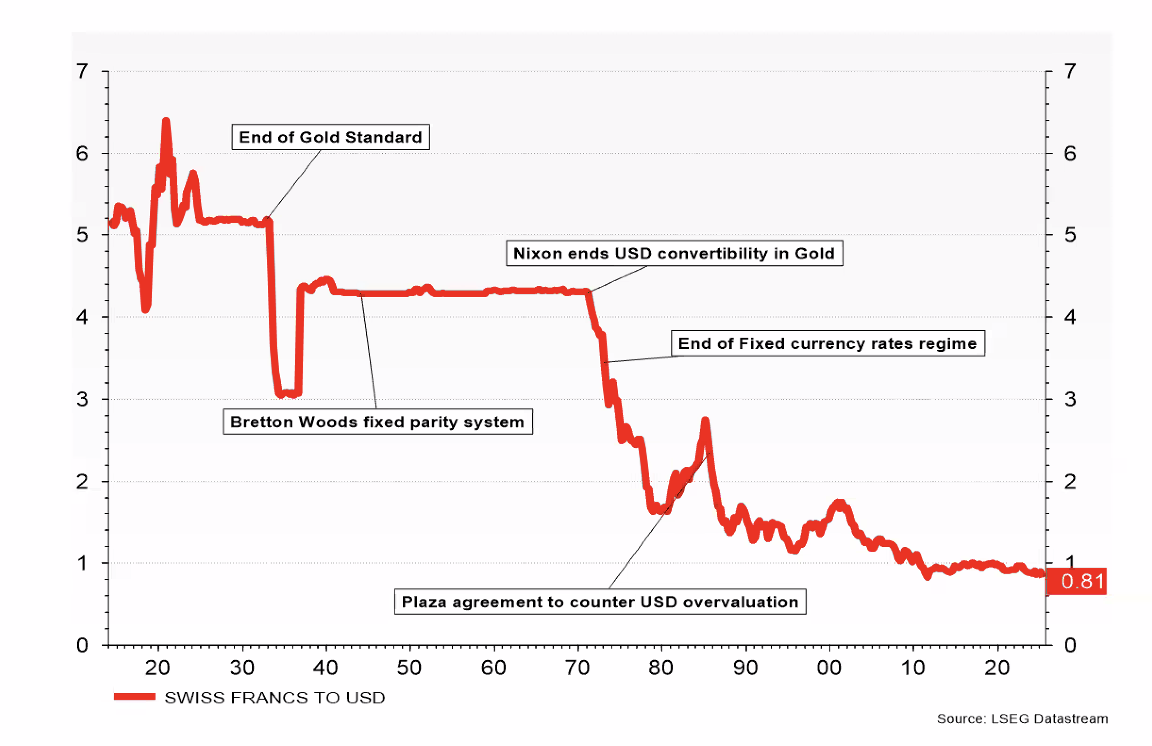

For American investors, this is a wake-up call. If U.S. policymakers themselves are openly advocating for a weaker dollar, then the decision to hold at least part of one’s wealth in foreign currencies should not be a difficult one.

So how is it possible that stock markets continue to signal “everything is fine” while central banks are acting as if the opposite were true? To us, the answer is that markets underestimate the difficulties facing the real economy. It is a dangerous game of musical chairs. At some point the music will stop, and when it does, not everyone will find a seat.

What tools will central banks have left then? With rates already low, their options are limited. They may once again resort to measures used in the past: massive purchases of equities and bonds, combined with direct cash transfers to households. Will it work? Perhaps in the short term. But it will almost certainly expand the money supply and risk reigniting inflation.

Our role is to help clients prepare for that moment—to structure portfolios so that when the music stops, they still have balance and stability, rather than volatility and regret.

A New Way Out

Another area where we see risks building is in how the U.S. finances its debt. With foreign investors less eager to buy Treasuries, Washington is looking for new ways to create demand. Enter the stablecoin. Under the recently passed GENIUS Act, institutions issuing stablecoins are required to back them primarily with U.S. Treasury bills. On the surface, this is presented as an exciting innovation in digital finance. In reality, it is simply another program designed to manufacture new buyers for U.S. debt.

The problem is obvious. If every stablecoin is backed by Treasuries, then for every existing U.S. dollar, another synthetic dollar can be created. It is essentially a second layer of leverage on the same debt. That may work for a while, but what happens if a major investor suddenly decides to redeem USD 100 billion worth of stablecoins? How stable will the coin be then? We do not have to look far back to remember how quickly financial institutions can collapse when confidence disappears—think of Silicon Valley Bank and the regional banking crisis just two years ago.

The Last Resort

Given these risks, it is worth returning to one of the oldest forms of wealth protection: precious metals. Gold, silver, and platinum have once again proven their role as a safe haven. Even when I personally thought gold might hit resistance, it continued to surprise on the upside. Silver has followed, and platinum is gaining new attention as well.

Of course, one has to be mindful of the point where a value trade becomes a momentum trade. But as we have said many times before, our focus is not on the short-term price moves of gold and silver. It is on their role in a long-term, generational investment strategy. Precious metals offer protection when currencies lose value, when inflation accelerates, and when geopolitical uncertainty rattles the system. They are not about speculation—they are about preservation.

Looking at all these developments from Switzerland, the conclusion is clear. The U.S. will remain an important market, but relying solely on it is dangerous. The risks are too concentrated, the policy path too unpredictable, and the dollar too vulnerable to political manipulation. By diversifying internationally—across currencies, regions, and asset classes—investors anchor their wealth more securely.

This is exactly what Switzerland offers: a stable financial system, a strong currency, political independence, and a long tradition of safeguarding wealth across generations. In a world where risks are rising, these qualities matter more than ever.

At WHVP, our mission is to help Americans take advantage of that. To step outside the echo chamber of U.S. markets, to look at the world through a different lens, and to build portfolios that can weather the storms ahead. We cannot control when the music stops. But we can make sure our clients still have a seat when it does.