While the World Watches the Games

The Winter Olympics in Italy are captivating audiences around the world. They offer moments of inspiration, discipline, and human achievement at the highest level. Yet beyond the spectacle, they also provide a useful reminder: success requires preparation, endurance, and financial discipline. Without it, even the most promising competitors falter.

Today, the global economic backdrop calls for similar caution. Ongoing geopolitical tensions, multiple regional conflicts, and—most notably—the unprecedented levels of sovereign debt across major economies deserve serious attention.

For years, we have highlighted the structural risks of continuously expanding government debt. The pace is accelerating. Based on U.S. Treasury data reported in March 2024, the United States was adding approximately one trillion dollars of new debt every 100 days. By October, according to the U.S. Congress Joint Economic Committee, that pace had quickened to just 71 days per trillion during the government shutdown period.

Equally concerning is the cost of servicing that debt. Roughly 20% of the U.S. federal budget is now allocated to interest payments alone. As debt levels rise, this burden compounds. The trajectory is difficult to reverse without meaningful fiscal reform. Whether the so-called “point of no return” lies ahead or has already been crossed is open to debate—but the direction of travel remains clear.

History offers perspective. The rise and decline of powerful states often followed similar patterns: growing financial obligations, political reluctance to impose discipline, and increasing reliance on debt issuance to fund expanding commitments. The story of Venice’s gradual decline in the 17th century is one example. While the contexts differ, the underlying lesson is timeless—debt used without restraint eventually limits flexibility and erodes stability.

Markets may continue to perform, and economies may prove resilient longer than many expect. But structural imbalances do not disappear on their own.

The Policy Balancing Act

The U.S., U.K., Japan, and the European Union each face meaningful—yet distinct—economic challenges. While debt and government spending connect them, the pace, structure, and market reactions differ.

The United Kingdom is navigating a difficult mix of tax policy changes, persistent inflation, and subdued growth. Business confidence remains cautious, and households continue to feel pressure from elevated living costs. At the same time, structural reform, if implemented decisively, could unlock meaningful economic potential. A more competitive, innovation-friendly environment would help restore momentum and attract long-term capital.

The European Union has made tangible progress in containing inflation, but growth remains constrained, partly due to regulatory complexity and slow structural adjustments. Should meaningful deregulation materialize, considerable untapped potential could be released. Recently signed trade agreements with South America and India may provide an additional tailwind by strengthening export channels and diversifying supply chains. Moreover, the bloc demonstrated notable unity during the Greenland dispute with the Trump administration. An encouraging although long overdue sign of political cohesion in the face of external pressure.

Japan presents a different dynamic. Prime Minister Sanae Takaichi has announced another fiscal spending package, adding to what is already the highest debt-to-GDP ratio among developed economies. Bond markets have reacted with caution. Further fiscal expansion risks renewed volatility in Japanese government bonds, potentially pushing yields higher. While structurally elevated debt is not a healthy long-term development, rising yields could eventually create tactical opportunities. At sufficiently attractive levels, investors may re-enter the Japanese bond market, supporting demand for the yen and potentially strengthening the currency in the short to mid-term.

The United States faces its own complexities. GDP growth has remained resilient, yet inflation continues to prove sticky. The announcement of a new Federal Reserve Chair adds another layer of uncertainty. Reports that China has encouraged its banks to reduce U.S. Treasury holdings in favor of gold illustrate a broader trend of gradual reserve diversification. The U.S. dollar is not collapsing, but global confidence appears to be slowly becoming less absolute. Currency stability ultimately reflects trust, and even a gradual shift in perception can influence purchasing power over time.

Across all major regions, economic growth continues to rely heavily on government spending. For investors, the overarching message remains clear: structural debt trends, fiscal discipline, and currency stability are central to long-term wealth preservation. In an environment where government spending is the primary driver of growth, thoughtful diversification across jurisdictions and currencies remains a prudent course of action.

Markets: Confidence or Complacency?

Markets entered 2026 on solid footing, although not without volatility. Large technology companies have moved between disappointment and renewed leadership as investors question elevated valuations. Japan’s equity markets have started the year strongly, while Europe has benefited from improved sentiment following new trade agreements and increasing political cohesion.

Optimism remains present, yet skepticism has not disappeared. U.S. consumers continue to spend, supported by a still-resilient labor market. At the same time, government spending remains elevated. Investors are attempting to determine whether the current expansion has further room to run or whether markets are becoming increasingly dependent on liquidity and policy support.

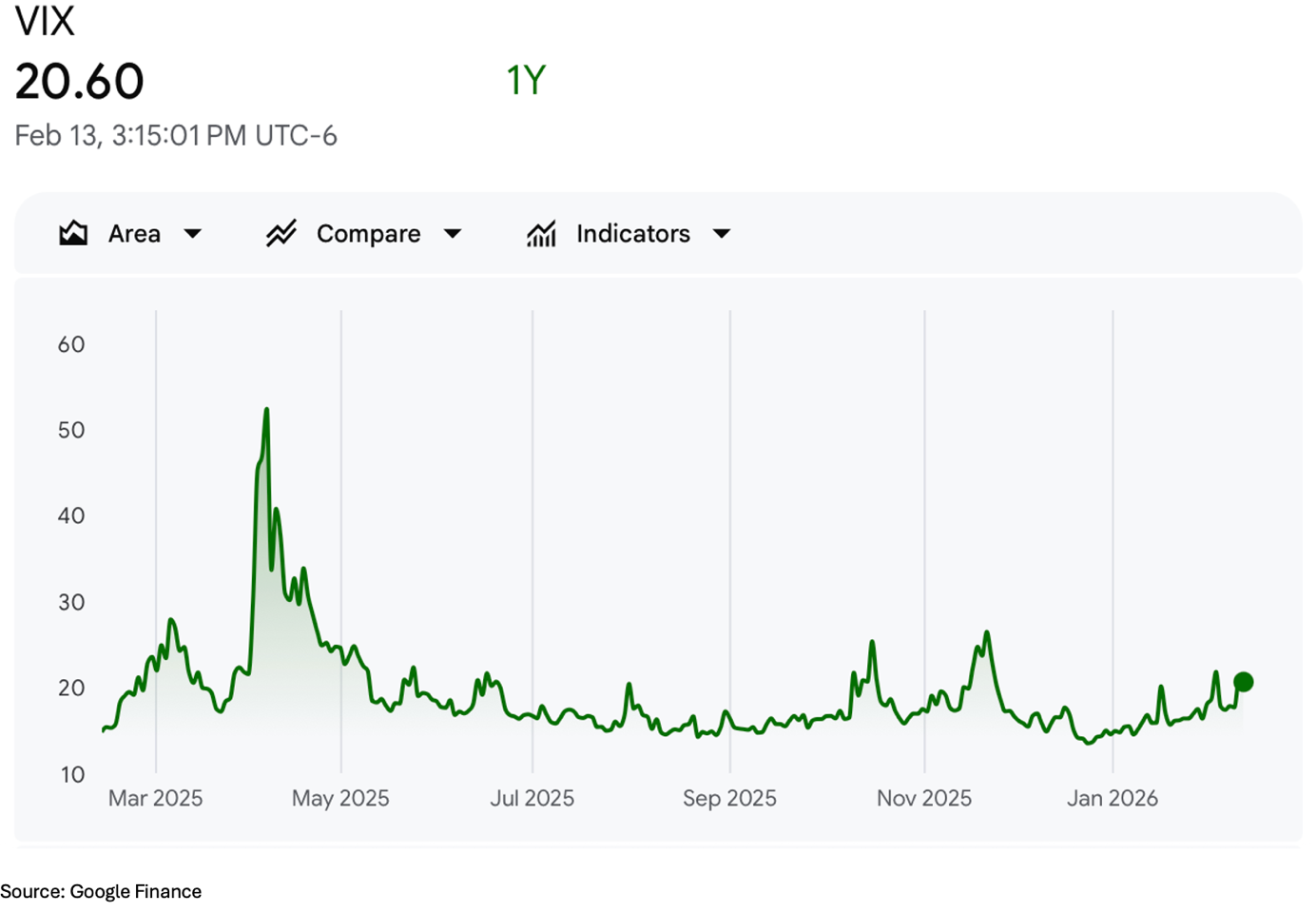

The VIX, often referred to as the market’s “fear gauge,” offers an interesting signal. While not near historic extremes, volatility has shown a noticeable uptick compared to much of last year. This suggests that beneath positive headline performance, uncertainty is building.

In this environment, two distinct mindsets are emerging. The first is what we would call cautious confidence. Markets remain structurally stable, capital is available, and selective opportunities exist. Liquidity is present, though investors are becoming more discerning. The second mindset leans toward complacency. Driven by a mixture of greed and fear of missing out. After three consecutive years of strong U.S. equity returns, some assume momentum will simply continue, particularly with the prospect of tax cuts, deregulation, and an administration perceived as market-friendly. While liquidity can sustain optimism longer than many expect, chasing momentum without regard to valuation or structural risk is rarely a durable strategy.

An important dynamic to watch is the evolving mechanism of liquidity itself. Traditionally, liquidity flows primarily through the Federal Reserve before finding its way into financial markets. However, alternative channels are being explored. One example is the concept of “Trump accounts” for children. With approximately 3.6 million births in the United States in 2025, a hypothetical $1,000 Treasury contribution per child would equate to $3.6 billion in initial funding alone. These accounts also allow for up to $5,000 in annual contributions from parents or even employers, meaning the total inflows could expand significantly over time.

Of course, not every child will have such an account, nor will every account receive maximum contributions. Nonetheless, even conservative participation assumptions could result in tens of billions of dollars flowing into markets annually. Relative to daily trading volumes, these sums are modest. Yet cumulatively, over years, they may become meaningful—both in supporting asset prices and in contributing to longer-term inflationary pressures.

Much like IRAs, these accounts may prove valuable tools for long-term wealth accumulation. At the same time, they represent a new, steady channel of capital formation—akin to a constant IV-drip into markets.

Fixed Income: Selectivity in a Shifting Environment

Selectivity defines today’s fixed income landscape. Not only in the United States, but globally. Increasingly, advisors are discussing the merits of de-risking portfolios and thoughtfully rebuilding bond allocations.

Whether driven by caution or simple normalization after years of strong equity performance, many investors recognize that rebalancing may be prudent. With inflation moderating across several regions, current yield levels offer an opportunity to lock in income. At the same time, central banks have adopted a more moderately dovish tone, supporting the case for fixed income.

That said, U.S. inflation remains somewhat sticky. Ongoing fiscal expansion and elevated government spending could prolong this dynamic, limiting how quickly rates can decline. In such an environment, duration exposure must be approached carefully.

In fixed income today, broad exposure is less compelling than disciplined selection. Quality, structure, and jurisdiction matter. For long-term wealth preservation, bonds are once again playing their traditional role, but prudence and global perspective remain essential.

Currencies: Where Confidence Resides, Strength Follows

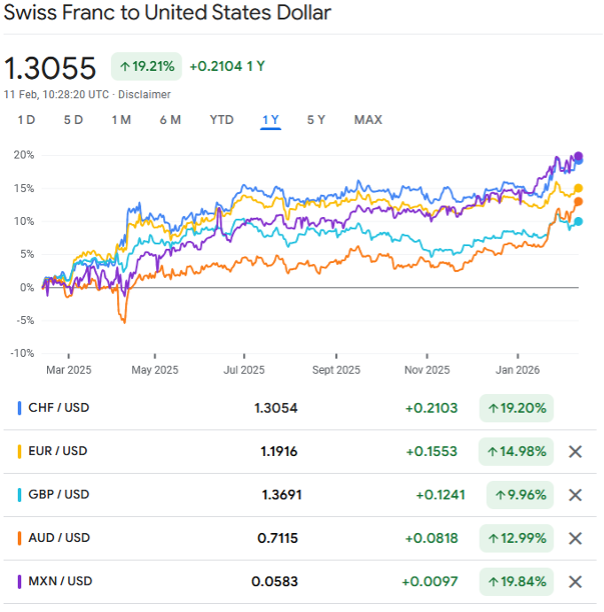

The U.S. Dollar Index (DXY) is down 1.55% year-to-date, following an approximate 8% decline in 2025. While this does not signal a disorderly move, the trend is notable, particularly in light of the dollar’s strength in prior years. Currency movements, however, are rarely uniform. The Swiss franc has appreciated roughly 19% year-over-year, while the euro has gained approximately 15% over the same period. Such divergences highlight how capital is reallocating selectively rather than exiting the dollar indiscriminately.

At present, currencies appear to reflect relative confidence in fiscal discipline and central bank credibility more than any tangible asset backing. In a world of fiat systems, trust is the anchor. Countries perceived as exercising greater spending control and monetary prudence were rewarded in 2025. Those pursuing more aggressive fiscal expansion experienced comparatively weaker currency performance.

Precious Metals: Consolidation

Precious metals started the year strong before correcting sharply at the end of January. The announcement of Kevin Warsh as incoming Fed Chair added volatility, but the selloff had multiple drivers.

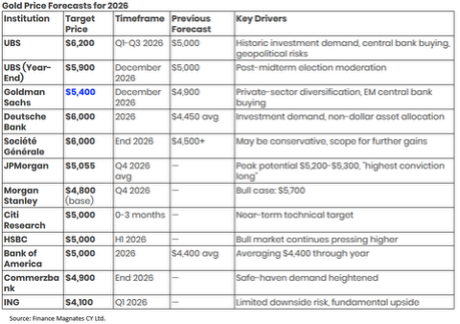

Outlooks for gold in 2026 remain mixed. Direction will likely depend on real interest rates, inflation trends, and central bank credibility. Despite short-term volatility, the broader case for precious metals as a hedge against currency risk and fiscal expansion remains intact.

Gold remains a valuable diversifier and deserves consideration within a portfolio. However, volatility is inherent. When fear and greed dominate, prudence is essential.

Closing Thoughts: The Discipline Advantage

As noted in our previous edition, equanimity matters more than excitement. The message may sound repetitive, but it remains essential.

One of the most striking qualities on display at the Olympic Games is composure under pressure. Athletes compete with clarity, discipline, and emotional control. What we rarely see are the setbacks, injuries, and difficult seasons that shaped their resilience long before they reached the global stage.

The same principle applies to investing. Periods of volatility test conviction. In such moments, it is vital to understand the strategy, ensure it aligns with long-term objectives, and remain steady under pressure. Sustainable success is built on discipline, not emotion.